Fiscal policy and inflation: A look at the American Rescue Plan’s impact and what it means for the Build Back Better Act

Inflation has jumped up beyond what many expected earlier in this year. While there are plenty of good reasons to think it will begin decelerating by early 2022 and settle into more normal ranges rather than continuing to spiral upward, it has already proven more stubborn than many (well, at least I) expected.

This raises two key questions: Does rising inflation mean critics of the American Rescue Plan (ARP) have been vindicated, as is often claimed lately? And does this mean that the Build Back Better Act (BBBA) currently being debate should be shelved and/or radically trimmed down in size?

The respective answers to these questions are “mostly not” and “absolutely not.”

Looking back on the American Rescue Plan debate

Back in February and March, center-left critics of the ARP claimed that it was too large and would lead to inflation. These critics made a very specific quantitative argument: The output gap—as estimated by the Congressional Budget Office (CBO)—was just –4% at the end of 2020, but the ARP would provide a fiscal impulse well over twice as large as that, leading to the output gap flipping quickly from negative to positive and sparking inflation. The output gap is essentially a proxy for how much aggregate demand (spending by households, businesses, and governments) lags behind the economy’s underlying productive capacity. More specifically, the output gap is the difference between actual gross domestic product (GDP) and potential GDP—with potential GDP being what the CBO estimates could be produced if the economy was operating with labor markets near the “natural rate” of unemployment.

In turn, the natural rate of unemployment is the lowest unemployment rate consistent with nonaccelerating inflation. If the unemployment rate stays below this natural rate for too long, the theory goes, then empowered workers will push wage growth high enough to put ever-growing upward pressure on prices. So potential GDP is what the economy could produce if labor was fully utilized in a sustainable (i.e., noninflationary) way. When actual GDP falls beneath this potential, it means aggregate demand is too slack and needs to be boosted. The ARP critics’ main claim was that the package provided far too large a boost given the size of the output gap in early 2021.

This was all a perfectly reasonable argument. The measured output gap was quite a bit smaller than the likely fiscal impulse of the ARP. I thought the overall argument was a bit too simple at the time, but it made some sense. Its main virtue was that it provided a crisp and inarguable empirical test that would allow us to check at a later date to see whether or not their scenario for why inflation would accelerate had actually come to pass.

So, did it?

No. Using the latest estimate of potential GDP (from July 2021), the output gap in the third quarter of 2021 remains negative (about –1.7%), even as inflation has jumped up considerably. This is just a fact.

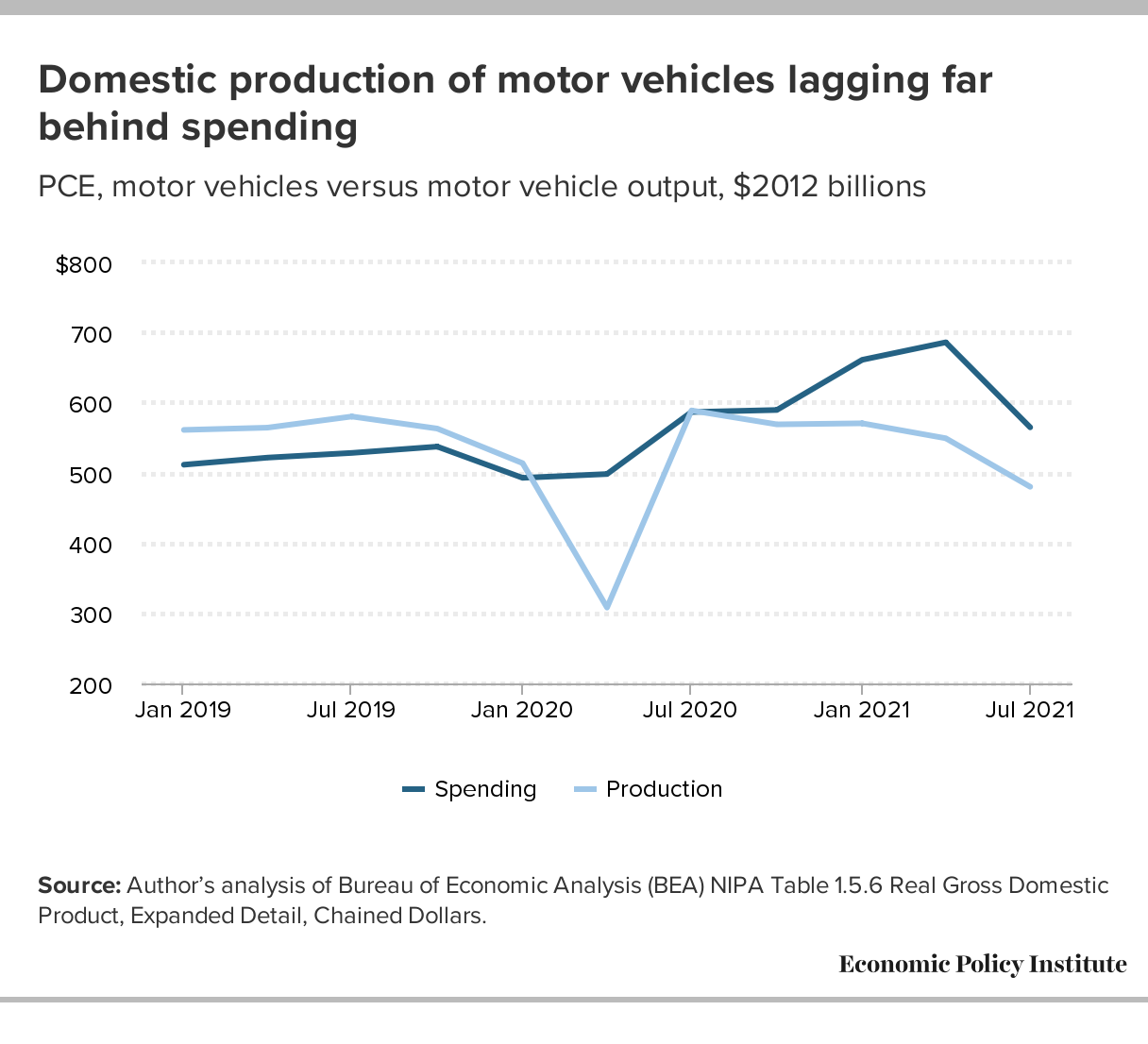

If the ARP critics were wrong about a rapid flip of the output gap from negative to positive, why has inflation accelerated? The very short answer is “COVID-19 never went away.” The longer answer is that the continuing presence of COVID-19 kept consumer spending highly skewed toward goods and away from face-to-face services even as overall GDP recovered rapidly, and COVID-19 shut down ports and shipping facilities around the world, severely stressing supply chains.

Could one say that an output gap in the goods sector flipped rapidly from negative to positive and that’s a big driver of the inflation we’ve seen? Yes! But that’s not the argument that ARP critics made. If they had said, “Consumer spending at the end of 2020 is extremely skewed toward goods. Even with relatively widespread vaccinations, this will not change much at all through the first half at least of 2021, so a large fiscal impulse would go into the goods sector in a historically unprecedented way. Supply chains will be almost unfathomably slow to respond to this,” that would have been genuinely prescient.

{kind=link}

Another plausible argument would have been that “CBO’s measure of potential output for 2021 is far too high (even though it had already been substantially marked down due to the effects of COVID-19 on the economy). Supply-chain dysfunction and the various ingredients causing pockets of shortages across the labor market actually make the productive capacity of the U.S. economy in 2021 far lower even than what it was in 2019.” Again, this seems likely right (though the reduction in productive capacity is likely to be quite short-lived), but it’s not what they said.

The argument that some ARP critics made that has come closest to being true is that the package might have been better if it had spread out the disbursement of fiscal relief and recovery measures more gradually over a longer period of time. I thought that was a solid argument at the time. In retrospect, however, because the aggregate output gap hasn’t closed as of September 2021, even as the ARP fiscal impulse has largely faded, I don’t think that too fast a disbursement of relief has been the big problem in generating inflation. The big problem, again, has been COVID-19 keeping services spending low and goods spending high while snarling supply chains.

If I could be transported back in time with the virtue of hindsight and given total control over the policymaking process surrounding the ARP, the real way to have better calibrated the package would have been to ensure spending on goods was supported gradually over the year while spending on services was boosted more rapidly. There’s no realistic way to do this, however. In theory, you could imagine a debit card given to all Americans that could be used only to buy goods, with a balance that started at $100 in the first month and then had progressively more money put on it in successive months, but with a bonus proportional to the balance carried over each month. This would have incentivized consumers to put off goods purchases as long as they could, but would also have signaled to goods producers that a wave of demand was coming their way—with enough lead time to better prepare for it. But all of this is obviously wildly unrealistic in many different ways.

Two last thoughts on this ARP retrospective:

First, as I note above, the best argument made in real time against the structure of ARP was about the pace of the spend-out. In practice, this was an argument against the stimulus checks included in it—they were by far the main reason why the ARP was so front-loaded. As I said at the time, the stimulus checks were not my favorite part of the ARP, but an odd set of political constellations aligned to make the checks nearly impossible to exclude (the short story is that promising the checks was a key campaign plank in the successful campaigns of both Democratic Georgia Senate candidates during January 2021). Given the inevitability of checks being included, the spend-out argument was not enough to say no to the full package.

Second, if we had simply “better calibrated” the ARP by spending less from January to September 2021, we would indeed have lower inflation today (goods spending would be lower and so would services spending). But we also wouldn’t have created the 5.8 million jobs seen so far in 2021, wage growth would be slower, and personal incomes would be lower. ARP critics pointing to current inflation want us to believe that a smaller ARP would have slowed only inflation but not the substantial improvements made in the economy over the past nine months. They’re wrong. As unhappy as I am about last month’s inflation numbers, I wouldn’t trade the 5.8 million jobs or higher personal incomes or faster wage growth for them.

Looking forward to the Build Back Better Act

While the retrospective look at the ARP is interesting, it’s also irrelevant to the policy question in front of us, which is, “Does the inflation spike provide any serious reason to trim back the BBBA package under debate?” It absolutely does not. Even many critics of (or at least worriers about) the ARP support the investments called for in the BBBA.

Further, unlike the ARP, the BBBA is tax-financed, not debt-financed. For good or bad, this blunts any inflationary impact it might have. Additionally, the overall structure of the BBBA’s spending is far less front-loaded than the ARP. The ARP was meant to provide immediate fiscal relief and stimulus. The BBBA is meant to address long-run investment shortfalls and safety net gaps in the U.S. economy. This means that in the long run, the BBBA is likely to boost the productive capacity of the U.S. economy and hopefully avoid supply-side crunches leading to inflationary spikes like we’ve seen. But, over the next year, the BBBA’s passage will not affect inflation one way or the other.

Finally, between the Federal Reserve’s announcement that it will decelerate its pace of buying bonds this month and the fact that that fiscal policy will make a sharp contractionary swing in 2022 (even if the BBBA is passed), there is already a big slowdown in aggregate demand support in front of us. There is no reason to prematurely pile on top of that. Even with recent months’ too-high inflation numbers, it remains true that an overreaction to inflationary episodes is often more damaging than the episode itself. Policymakers should avoid this.

Enjoyed this post?

Sign up for EPI's newsletter so you never miss our research and insights on ways to make the economy work better for everyone.