Southern state policymakers must do more to respond to the coronavirus pandemic: Medicaid expansion, emergency paid sick leave, and dedicated public health resources are especially needed

This piece is the first in a three-part series examining the economic and social conditions that impact health outcomes in Southern states, and how these conditions leave communities underprepared to protect frontline workers and communities during the pandemic.

U.S. federal lawmakers are poised to pass a stimulus package to combat the coronavirus pandemic’s public health and economic damage. In a recent post, we laid out the critical steps that state and local lawmakers should take to protect workers and families, slow the spread of the virus, and mitigate its economic toll. This piece will highlight how state and local policymakers in the Southern states are responding to the crisis, and what more is needed.

Health organizations broadly recognize that where we live and work impacts health risks and health outcomes. By recognizing the economic and social conditions that influence health equity for people living in Southern states, policymakers can provide more targeted solutions to protect public health and support families already struggling to make ends meet.

Nurses in garbage bags?: Why the Trump administration must use the Defense Production Act to mobilize production of critically needed hospital protective equipment immediately

On Tuesday, New York Governor Andrew Cuomo spent much of his coronavirus press conference imploring President Trump to use the Defense Production Act (DPA) now to force factories to manufacture essential medical equipment such as masks, gloves, gowns, and ventilators.

Trump has continually refused to do so, saying that the acquisition of medical supplies is a job for governors: “You know, we’re not a shipping clerk.” Yet, on a conference call last week, Republican governor Charlie Baker (Mass.) told Trump that his state had been denied three major orders for medical equipment because the federal government had outbid him.

Health care workers are at the front lines of the COVID-19 crisis. In Italy, 9% of “total COVID-19 cases are health care workers, contributing to the breakdown of the hospital system in the north of the country.” U.S. health care workers are also especially hard hit.

While both Democratic and Republican governors are pleading for help, staff in at least one nursing home have already resorted to using plastic garbage bags to make gowns, as have nurses and doctors in Spain and England.

Clearly, the DPA will make a difference.Read more

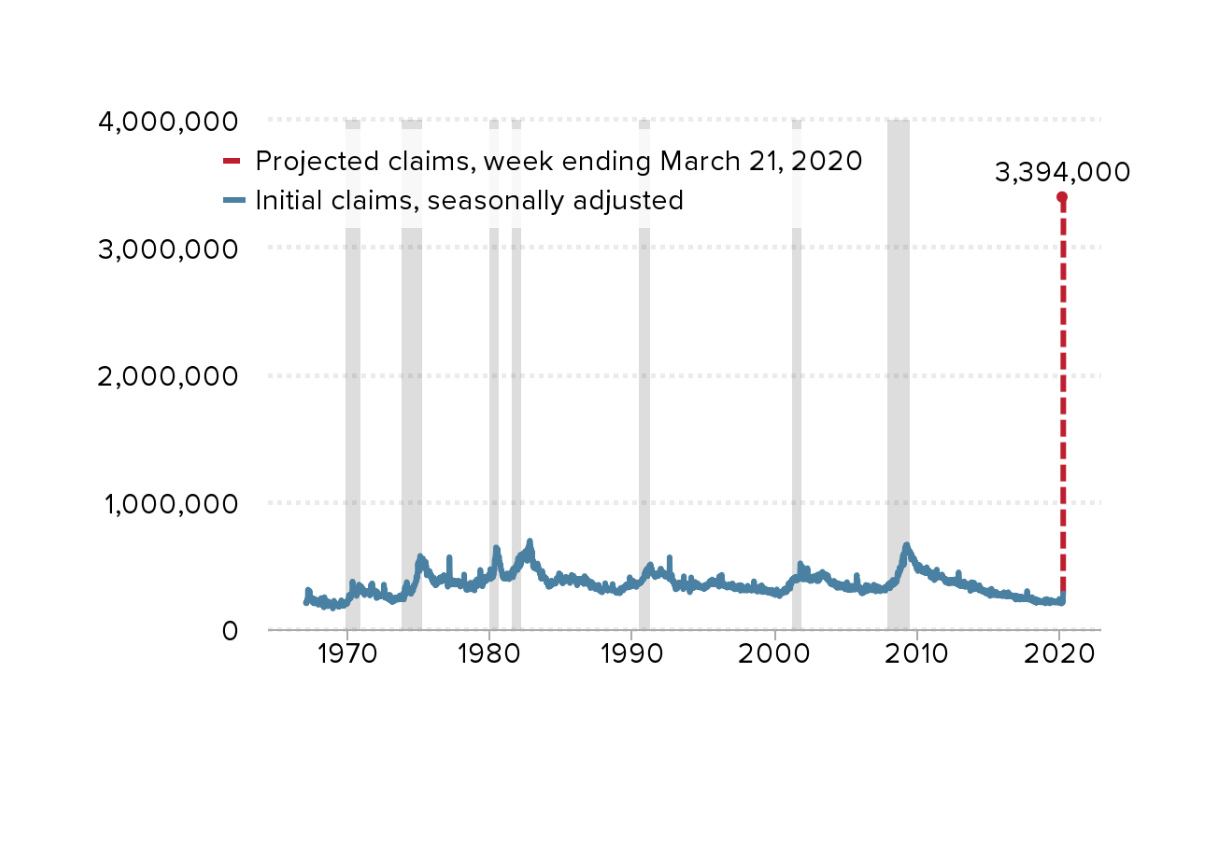

The coronavirus crisis led to a record-breaking spike in weekly unemployment insurance claims: An estimated 3.4 million workers filed for unemployment last week

A greater share of Americans filed for unemployment insurance in the week ending March 21 than in any prior week in American history, according to our analysis of news reports.

Many states reported initial claims growth of over 1,000%. Our model predicts that 3.4 million Americans filed new claims for unemployment insurance this past week, although we believe that number could be as low as 3 million or could be substantially higher. This will dwarf every other week in history, as can be seen by comparing the projection against the trend in initial claims back to 1967 (Figure A).

The U.S. is experiencing a record-breaking spike in unemployment: Initial weekly unemployment claims since 1967 and projected claims for the week ending March 21, 2020

| Week ending date | Initial claims, seasonally adjusted | Projected claims, week ending March 21, 2020 |

|---|---|---|

| 1967-01-07 | 208000 | |

| 1967-01-14 | 207000 | |

| 1967-01-21 | 217000 | |

| 1967-01-28 | 204000 | |

| 1967-02-04 | 216000 | |

| 1967-02-11 | 229000 | |

| 1967-02-18 | 229000 | |

| 1967-02-25 | 242000 | |

| 1967-03-04 | 310000 | |

| 1967-03-11 | 241000 | |

| 1967-03-18 | 245000 | |

| 1967-03-25 | 247000 | |

| 1967-04-01 | 259000 | |

| 1967-04-08 | 257000 | |

| 1967-04-15 | 299000 | |

| 1967-04-22 | 245000 | |

| 1967-04-29 | 255000 | |

| 1967-05-06 | 254000 | |

| 1967-05-13 | 231000 | |

| 1967-05-20 | 230000 | |

| 1967-05-27 | 228000 | |

| 1967-06-03 | 248000 | |

| 1967-06-10 | 238000 | |

| 1967-06-17 | 224000 | |

| 1967-06-24 | 218000 | |

| 1967-07-01 | 209000 | |

| 1967-07-08 | 240000 | |

| 1967-07-15 | 241000 | |

| 1967-07-22 | 240000 | |

| 1967-07-29 | 209000 | |

| 1967-08-05 | 221000 | |

| 1967-08-12 | 202000 | |

| 1967-08-19 | 215000 | |

| 1967-08-26 | 213000 | |

| 1967-09-02 | 218000 | |

| 1967-09-09 | 231000 | |

| 1967-09-16 | 220000 | |

| 1967-09-23 | 209000 | |

| 1967-09-30 | 204000 | |

| 1967-10-07 | 231000 | |

| 1967-10-14 | 206000 | |

| 1967-10-21 | 223000 | |

| 1967-10-28 | 207000 | |

| 1967-11-04 | 222000 | |

| 1967-11-11 | 214000 | |

| 1967-11-18 | 198000 | |

| 1967-11-25 | 191000 | |

| 1967-12-02 | 196000 | |

| 1967-12-09 | 221000 | |

| 1967-12-16 | 204000 | |

| 1967-12-23 | 219000 | |

| 1967-12-30 | 216000 | |

| 1968-01-06 | 222000 | |

| 1968-01-13 | 222000 | |

| 1968-01-20 | 221000 | |

| 1968-01-27 | 198000 | |

| 1968-02-03 | 244000 | |

| 1968-02-10 | 210000 | |

| 1968-02-17 | 196000 | |

| 1968-02-24 | 193000 | |

| 1968-03-02 | 190000 | |

| 1968-03-09 | 204000 | |

| 1968-03-16 | 190000 | |

| 1968-03-23 | 200000 | |

| 1968-03-30 | 192000 | |

| 1968-04-06 | 191000 | |

| 1968-04-13 | 171000 | |

| 1968-04-20 | 183000 | |

| 1968-04-27 | 251000 | |

| 1968-05-04 | 209000 | |

| 1968-05-11 | 194000 | |

| 1968-05-18 | 199000 | |

| 1968-05-25 | 194000 | |

| 1968-06-01 | 199000 | |

| 1968-06-08 | 192000 | |

| 1968-06-15 | 194000 | |

| 1968-06-22 | 189000 | |

| 1968-06-29 | 194000 | |

| 1968-07-06 | 214000 | |

| 1968-07-13 | 186000 | |

| 1968-07-20 | 180000 | |

| 1968-07-27 | 205000 | |

| 1968-08-03 | 206000 | |

| 1968-08-10 | 218000 | |

| 1968-08-17 | 192000 | |

| 1968-08-24 | 193000 | |

| 1968-08-31 | 188000 | |

| 1968-09-07 | 189000 | |

| 1968-09-14 | 195000 | |

| 1968-09-21 | 191000 | |

| 1968-09-28 | 189000 | |

| 1968-10-05 | 185000 | |

| 1968-10-12 | 186000 | |

| 1968-10-19 | 191000 | |

| 1968-10-26 | 182000 | |

| 1968-11-02 | 181000 | |

| 1968-11-09 | 183000 | |

| 1968-11-16 | 192000 | |

| 1968-11-23 | 199000 | |

| 1968-11-30 | 162000 | |

| 1968-12-07 | 188000 | |

| 1968-12-14 | 195000 | |

| 1968-12-21 | 192000 | |

| 1968-12-28 | 223000 | |

| 1969-01-04 | 190000 | |

| 1969-01-11 | 191000 | |

| 1969-01-18 | 192000 | |

| 1969-01-25 | 193000 | |

| 1969-02-01 | 203000 | |

| 1969-02-08 | 197000 | |

| 1969-02-15 | 192000 | |

| 1969-02-22 | 192000 | |

| 1969-03-01 | 201000 | |

| 1969-03-08 | 191000 | |

| 1969-03-15 | 189000 | |

| 1969-03-22 | 181000 | |

| 1969-03-29 | 183000 | |

| 1969-04-05 | 182000 | |

| 1969-04-12 | 190000 | |

| 1969-04-19 | 187000 | |

| 1969-04-26 | 177000 | |

| 1969-05-03 | 177000 | |

| 1969-05-10 | 183000 | |

| 1969-05-17 | 179000 | |

| 1969-05-24 | 180000 | |

| 1969-05-31 | 187000 | |

| 1969-06-07 | 192000 | |

| 1969-06-14 | 182000 | |

| 1969-06-21 | 191000 | |

| 1969-06-28 | 203000 | |

| 1969-07-05 | 227000 | |

| 1969-07-12 | 210000 | |

| 1969-07-19 | 206000 | |

| 1969-07-26 | 192000 | |

| 1969-08-02 | 196000 | |

| 1969-08-09 | 203000 | |

| 1969-08-16 | 199000 | |

| 1969-08-23 | 199000 | |

| 1969-08-30 | 195000 | |

| 1969-09-06 | 182000 | |

| 1969-09-13 | 209000 | |

| 1969-09-20 | 195000 | |

| 1969-09-27 | 193000 | |

| 1969-10-04 | 193000 | |

| 1969-10-11 | 200000 | |

| 1969-10-18 | 199000 | |

| 1969-10-25 | 205000 | |

| 1969-11-01 | 198000 | |

| 1969-11-08 | 211000 | |

| 1969-11-15 | 197000 | |

| 1969-11-22 | 217000 | |

| 1969-11-29 | 202000 | |

| 1969-12-06 | 202000 | |

| 1969-12-13 | 222000 | |

| 1969-12-20 | 232000 | |

| 1969-12-27 | 223000 | |

| 1970-01-03 | 230000 | |

| 1970-01-10 | 242000 | |

| 1970-01-17 | 268000 | |

| 1970-01-24 | 256000 | |

| 1970-01-31 | 239000 | |

| 1970-02-07 | 256000 | |

| 1970-02-14 | 265000 | |

| 1970-02-21 | 271000 | |

| 1970-02-28 | 242000 | |

| 1970-03-07 | 262000 | |

| 1970-03-14 | 271000 | |

| 1970-03-21 | 264000 | |

| 1970-03-28 | 276000 | |

| 1970-04-04 | 273000 | |

| 1970-04-11 | 305000 | |

| 1970-04-18 | 374000 | |

| 1970-04-25 | 349000 | |

| 1970-05-02 | 334000 | |

| 1970-05-09 | 318000 | |

| 1970-05-16 | 303000 | |

| 1970-05-23 | 296000 | |

| 1970-05-30 | 301000 | |

| 1970-06-06 | 301000 | |

| 1970-06-13 | 298000 | |

| 1970-06-20 | 296000 | |

| 1970-06-27 | 291000 | |

| 1970-07-04 | 277000 | |

| 1970-07-11 | 288000 | |

| 1970-07-18 | 294000 | |

| 1970-07-25 | 287000 | |

| 1970-08-01 | 261000 | |

| 1970-08-08 | 266000 | |

| 1970-08-15 | 300000 | |

| 1970-08-22 | 303000 | |

| 1970-08-29 | 297000 | |

| 1970-09-05 | 324000 | |

| 1970-09-12 | 292000 | |

| 1970-09-19 | 325000 | |

| 1970-09-26 | 333000 | |

| 1970-10-03 | 350000 | |

| 1970-10-10 | 327000 | |

| 1970-10-17 | 334000 | |

| 1970-10-24 | 330000 | |

| 1970-10-31 | 327000 | |

| 1970-11-07 | 336000 | |

| 1970-11-14 | 314000 | |

| 1970-11-21 | 314000 | |

| 1970-11-28 | 337000 | |

| 1970-12-05 | 308000 | |

| 1970-12-12 | 306000 | |

| 1970-12-19 | 289000 | |

| 1970-12-26 | 321000 | |

| 1971-01-02 | 303000 | |

| 1971-01-09 | 288000 | |

| 1971-01-16 | 299000 | |

| 1971-01-23 | 312000 | |

| 1971-01-30 | 292000 | |

| 1971-02-06 | 296000 | |

| 1971-02-13 | 282000 | |

| 1971-02-20 | 268000 | |

| 1971-02-27 | 290000 | |

| 1971-03-06 | 297000 | |

| 1971-03-13 | 287000 | |

| 1971-03-20 | 291000 | |

| 1971-03-27 | 300000 | |

| 1971-04-03 | 299000 | |

| 1971-04-10 | 279000 | |

| 1971-04-17 | 284000 | |

| 1971-04-24 | 288000 | |

| 1971-05-01 | 290000 | |

| 1971-05-08 | 293000 | |

| 1971-05-15 | 284000 | |

| 1971-05-22 | 295000 | |

| 1971-05-29 | 299000 | |

| 1971-06-05 | 301000 | |

| 1971-06-12 | 295000 | |

| 1971-06-19 | 299000 | |

| 1971-06-26 | 291000 | |

| 1971-07-03 | 277000 | |

| 1971-07-10 | 264000 | |

| 1971-07-17 | 313000 | |

| 1971-07-24 | 304000 | |

| 1971-07-31 | 308000 | |

| 1971-08-07 | 349000 | |

| 1971-08-14 | 325000 | |

| 1971-08-21 | 320000 | |

| 1971-08-28 | 307000 | |

| 1971-09-04 | 359000 | |

| 1971-09-11 | 312000 | |

| 1971-09-18 | 302000 | |

| 1971-09-25 | 308000 | |

| 1971-10-02 | 299000 | |

| 1971-10-09 | 313000 | |

| 1971-10-16 | 299000 | |

| 1971-10-23 | 294000 | |

| 1971-10-30 | 283000 | |

| 1971-11-06 | 301000 | |

| 1971-11-13 | 295000 | |

| 1971-11-20 | 274000 | |

| 1971-11-27 | 278000 | |

| 1971-12-04 | 299000 | |

| 1971-12-11 | 280000 | |

| 1971-12-18 | 269000 | |

| 1971-12-25 | 244000 | |

| 1972-01-01 | 279000 | |

| 1972-01-08 | 295000 | |

| 1972-01-15 | 250000 | |

| 1972-01-22 | 263000 | |

| 1972-01-29 | 269000 | |

| 1972-02-05 | 276000 | |

| 1972-02-12 | 266000 | |

| 1972-02-19 | 258000 | |

| 1972-02-26 | 254000 | |

| 1972-03-04 | 257000 | |

| 1972-03-11 | 264000 | |

| 1972-03-18 | 266000 | |

| 1972-03-25 | 264000 | |

| 1972-04-01 | 258000 | |

| 1972-04-08 | 274000 | |

| 1972-04-15 | 259000 | |

| 1972-04-22 | 259000 | |

| 1972-04-29 | 265000 | |

| 1972-05-06 | 271000 | |

| 1972-05-13 | 266000 | |

| 1972-05-20 | 267000 | |

| 1972-05-27 | 267000 | |

| 1972-06-03 | 264000 | |

| 1972-06-10 | 268000 | |

| 1972-06-17 | 275000 | |

| 1972-06-24 | 286000 | |

| 1972-07-01 | 350000 | |

| 1972-07-08 | 297000 | |

| 1972-07-15 | 318000 | |

| 1972-07-22 | 276000 | |

| 1972-07-29 | 247000 | |

| 1972-08-05 | 250000 | |

| 1972-08-12 | 246000 | |

| 1972-08-19 | 256000 | |

| 1972-08-26 | 262000 | |

| 1972-09-02 | 258000 | |

| 1972-09-09 | 259000 | |

| 1972-09-16 | 258000 | |

| 1972-09-23 | 255000 | |

| 1972-09-30 | 251000 | |

| 1972-10-07 | 263000 | |

| 1972-10-14 | 250000 | |

| 1972-10-21 | 257000 | |

| 1972-10-28 | 234000 | |

| 1972-11-04 | 255000 | |

| 1972-11-11 | 242000 | |

| 1972-11-18 | 271000 | |

| 1972-11-25 | 235000 | |

| 1972-12-02 | 226000 | |

| 1972-12-09 | 252000 | |

| 1972-12-16 | 263000 | |

| 1972-12-23 | 246000 | |

| 1972-12-30 | 225000 | |

| 1973-01-06 | 226000 | |

| 1973-01-13 | 245000 | |

| 1973-01-20 | 229000 | |

| 1973-01-27 | 214000 | |

| 1973-02-03 | 228000 | |

| 1973-02-10 | 226000 | |

| 1973-02-17 | 216000 | |

| 1973-02-24 | 218000 | |

| 1973-03-03 | 225000 | |

| 1973-03-10 | 229000 | |

| 1973-03-17 | 228000 | |

| 1973-03-24 | 232000 | |

| 1973-03-31 | 222000 | |

| 1973-04-07 | 247000 | |

| 1973-04-14 | 230000 | |

| 1973-04-21 | 243000 | |

| 1973-04-28 | 236000 | |

| 1973-05-05 | 248000 | |

| 1973-05-12 | 238000 | |

| 1973-05-19 | 237000 | |

| 1973-05-26 | 238000 | |

| 1973-06-02 | 232000 | |

| 1973-06-09 | 246000 | |

| 1973-06-16 | 237000 | |

| 1973-06-23 | 242000 | |

| 1973-06-30 | 237000 | |

| 1973-07-07 | 248000 | |

| 1973-07-14 | 232000 | |

| 1973-07-21 | 241000 | |

| 1973-07-28 | 250000 | |

| 1973-08-04 | 256000 | |

| 1973-08-11 | 265000 | |

| 1973-08-18 | 258000 | |

| 1973-08-25 | 254000 | |

| 1973-09-01 | 242000 | |

| 1973-09-08 | 252000 | |

| 1973-09-15 | 245000 | |

| 1973-09-22 | 246000 | |

| 1973-09-29 | 249000 | |

| 1973-10-06 | 236000 | |

| 1973-10-13 | 246000 | |

| 1973-10-20 | 249000 | |

| 1973-10-27 | 235000 | |

| 1973-11-03 | 246000 | |

| 1973-11-10 | 282000 | |

| 1973-11-17 | 254000 | |

| 1973-11-24 | 233000 | |

| 1973-12-01 | 256000 | |

| 1973-12-08 | 266000 | |

| 1973-12-15 | 272000 | |

| 1973-12-22 | 326000 | |

| 1973-12-29 | 300000 | |

| 1974-01-05 | 269000 | |

| 1974-01-12 | 340000 | |

| 1974-01-19 | 321000 | |

| 1974-01-26 | 291000 | |

| 1974-02-02 | 302000 | |

| 1974-02-09 | 369000 | |

| 1974-02-16 | 311000 | |

| 1974-02-23 | 292000 | |

| 1974-03-02 | 301000 | |

| 1974-03-09 | 305000 | |

| 1974-03-16 | 315000 | |

| 1974-03-23 | 314000 | |

| 1974-03-30 | 323000 | |

| 1974-04-06 | 296000 | |

| 1974-04-13 | 297000 | |

| 1974-04-20 | 296000 | |

| 1974-04-27 | 283000 | |

| 1974-05-04 | 287000 | |

| 1974-05-11 | 296000 | |

| 1974-05-18 | 298000 | |

| 1974-05-25 | 309000 | |

| 1974-06-01 | 278000 | |

| 1974-06-08 | 314000 | |

| 1974-06-15 | 303000 | |

| 1974-06-22 | 308000 | |

| 1974-06-29 | 325000 | |

| 1974-07-06 | 311000 | |

| 1974-07-13 | 304000 | |

| 1974-07-20 | 303000 | |

| 1974-07-27 | 320000 | |

| 1974-08-03 | 335000 | |

| 1974-08-10 | 347000 | |

| 1974-08-17 | 332000 | |

| 1974-08-24 | 343000 | |

| 1974-08-31 | 350000 | |

| 1974-09-07 | 350000 | |

| 1974-09-14 | 357000 | |

| 1974-09-21 | 370000 | |

| 1974-09-28 | 366000 | |

| 1974-10-05 | 371000 | |

| 1974-10-12 | 413000 | |

| 1974-10-19 | 389000 | |

| 1974-10-26 | 414000 | |

| 1974-11-02 | 406000 | |

| 1974-11-09 | 441000 | |

| 1974-11-16 | 449000 | |

| 1974-11-23 | 518000 | |

| 1974-11-30 | 474000 | |

| 1974-12-07 | 528000 | |

| 1974-12-14 | 510000 | |

| 1974-12-21 | 521000 | |

| 1974-12-28 | 537000 | |

| 1975-01-04 | 456000 | |

| 1975-01-11 | 554000 | |

| 1975-01-18 | 575000 | |

| 1975-01-25 | 555000 | |

| 1975-02-01 | 559000 | |

| 1975-02-08 | 545000 | |

| 1975-02-15 | 530000 | |

| 1975-02-22 | 544000 | |

| 1975-03-01 | 546000 | |

| 1975-03-08 | 551000 | |

| 1975-03-15 | 531000 | |

| 1975-03-22 | 550000 | |

| 1975-03-29 | 555000 | |

| 1975-04-05 | 537000 | |

| 1975-04-12 | 520000 | |

| 1975-04-19 | 531000 | |

| 1975-04-26 | 513000 | |

| 1975-05-03 | 505000 | |

| 1975-05-10 | 507000 | |

| 1975-05-17 | 514000 | |

| 1975-05-24 | 493000 | |

| 1975-05-31 | 475000 | |

| 1975-06-07 | 529000 | |

| 1975-06-14 | 497000 | |

| 1975-06-21 | 497000 | |

| 1975-06-28 | 459000 | |

| 1975-07-05 | 423000 | |

| 1975-07-12 | 446000 | |

| 1975-07-19 | 445000 | |

| 1975-07-26 | 454000 | |

| 1975-08-02 | 454000 | |

| 1975-08-09 | 459000 | |

| 1975-08-16 | 444000 | |

| 1975-08-23 | 457000 | |

| 1975-08-30 | 446000 | |

| 1975-09-06 | 447000 | |

| 1975-09-13 | 456000 | |

| 1975-09-20 | 433000 | |

| 1975-09-27 | 445000 | |

| 1975-10-04 | 426000 | |

| 1975-10-11 | 429000 | |

| 1975-10-18 | 404000 | |

| 1975-10-25 | 426000 | |

| 1975-11-01 | 414000 | |

| 1975-11-08 | 415000 | |

| 1975-11-15 | 386000 | |

| 1975-11-22 | 401000 | |

| 1975-11-29 | 387000 | |

| 1975-12-06 | 373000 | |

| 1975-12-13 | 368000 | |

| 1975-12-20 | 365000 | |

| 1975-12-27 | 391000 | |

| 1976-01-03 | 362000 | |

| 1976-01-10 | 402000 | |

| 1976-01-17 | 370000 | |

| 1976-01-24 | 363000 | |

| 1976-01-31 | 359000 | |

| 1976-02-07 | 353000 | |

| 1976-02-14 | 344000 | |

| 1976-02-21 | 347000 | |

| 1976-02-28 | 349000 | |

| 1976-03-06 | 348000 | |

| 1976-03-13 | 360000 | |

| 1976-03-20 | 368000 | |

| 1976-03-27 | 366000 | |

| 1976-04-03 | 380000 | |

| 1976-04-10 | 373000 | |

| 1976-04-17 | 361000 | |

| 1976-04-24 | 367000 | |

| 1976-05-01 | 385000 | |

| 1976-05-08 | 395000 | |

| 1976-05-15 | 382000 | |

| 1976-05-22 | 394000 | |

| 1976-05-29 | 402000 | |

| 1976-06-05 | 382000 | |

| 1976-06-12 | 407000 | |

| 1976-06-19 | 399000 | |

| 1976-06-26 | 387000 | |

| 1976-07-03 | 394000 | |

| 1976-07-10 | 372000 | |

| 1976-07-17 | 406000 | |

| 1976-07-24 | 394000 | |

| 1976-07-31 | 388000 | |

| 1976-08-07 | 378000 | |

| 1976-08-14 | 382000 | |

| 1976-08-21 | 400000 | |

| 1976-08-28 | 394000 | |

| 1976-09-04 | 421000 | |

| 1976-09-11 | 383000 | |

| 1976-09-18 | 403000 | |

| 1976-09-25 | 423000 | |

| 1976-10-02 | 408000 | |

| 1976-10-09 | 411000 | |

| 1976-10-16 | 403000 | |

| 1976-10-23 | 409000 | |

| 1976-10-30 | 414000 | |

| 1976-11-06 | 390000 | |

| 1976-11-13 | 383000 | |

| 1976-11-20 | 408000 | |

| 1976-11-27 | 377000 | |

| 1976-12-04 | 402000 | |

| 1976-12-11 | 395000 | |

| 1976-12-18 | 365000 | |

| 1976-12-25 | 333000 | |

| 1977-01-01 | 380000 | |

| 1977-01-08 | 416000 | |

| 1977-01-15 | 368000 | |

| 1977-01-22 | 423000 | |

| 1977-01-29 | 422000 | |

| 1977-02-05 | 565000 | |

| 1977-02-12 | 477000 | |

| 1977-02-19 | 399000 | |

| 1977-02-26 | 362000 | |

| 1977-03-05 | 361000 | |

| 1977-03-12 | 355000 | |

| 1977-03-19 | 369000 | |

| 1977-03-26 | 356000 | |

| 1977-04-02 | 350000 | |

| 1977-04-09 | 376000 | |

| 1977-04-16 | 361000 | |

| 1977-04-23 | 375000 | |

| 1977-04-30 | 375000 | |

| 1977-05-07 | 384000 | |

| 1977-05-14 | 381000 | |

| 1977-05-21 | 375000 | |

| 1977-05-28 | 381000 | |

| 1977-06-04 | 363000 | |

| 1977-06-11 | 358000 | |

| 1977-06-18 | 359000 | |

| 1977-06-25 | 365000 | |

| 1977-07-02 | 350000 | |

| 1977-07-09 | 361000 | |

| 1977-07-16 | 366000 | |

| 1977-07-23 | 365000 | |

| 1977-07-30 | 365000 | |

| 1977-08-06 | 378000 | |

| 1977-08-13 | 359000 | |

| 1977-08-20 | 367000 | |

| 1977-08-27 | 365000 | |

| 1977-09-03 | 374000 | |

| 1977-09-10 | 359000 | |

| 1977-09-17 | 362000 | |

| 1977-09-24 | 380000 | |

| 1977-10-01 | 348000 | |

| 1977-10-08 | 365000 | |

| 1977-10-15 | 358000 | |

| 1977-10-22 | 375000 | |

| 1977-10-29 | 349000 | |

| 1977-11-05 | 366000 | |

| 1977-11-12 | 334000 | |

| 1977-11-19 | 360000 | |

| 1977-11-26 | 354000 | |

| 1977-12-03 | 367000 | |

| 1977-12-10 | 364000 | |

| 1977-12-17 | 359000 | |

| 1977-12-24 | 344000 | |

| 1977-12-31 | 364000 | |

| 1978-01-07 | 346000 | |

| 1978-01-14 | 343000 | |

| 1978-01-21 | 352000 | |

| 1978-01-28 | 363000 | |

| 1978-02-04 | 360000 | |

| 1978-02-11 | 373000 | |

| 1978-02-18 | 429000 | |

| 1978-02-25 | 371000 | |

| 1978-03-04 | 355000 | |

| 1978-03-11 | 359000 | |

| 1978-03-18 | 347000 | |

| 1978-03-25 | 335000 | |

| 1978-04-01 | 333000 | |

| 1978-04-08 | 345000 | |

| 1978-04-15 | 309000 | |

| 1978-04-22 | 319000 | |

| 1978-04-29 | 324000 | |

| 1978-05-06 | 334000 | |

| 1978-05-13 | 322000 | |

| 1978-05-20 | 334000 | |

| 1978-05-27 | 318000 | |

| 1978-06-03 | 310000 | |

| 1978-06-10 | 331000 | |

| 1978-06-17 | 326000 | |

| 1978-06-24 | 330000 | |

| 1978-07-01 | 348000 | |

| 1978-07-08 | 356000 | |

| 1978-07-15 | 352000 | |

| 1978-07-22 | 349000 | |

| 1978-07-29 | 346000 | |

| 1978-08-05 | 365000 | |

| 1978-08-12 | 354000 | |

| 1978-08-19 | 343000 | |

| 1978-08-26 | 333000 | |

| 1978-09-02 | 313000 | |

| 1978-09-09 | 337000 | |

| 1978-09-16 | 322000 | |

| 1978-09-23 | 323000 | |

| 1978-09-30 | 318000 | |

| 1978-10-07 | 343000 | |

| 1978-10-14 | 316000 | |

| 1978-10-21 | 338000 | |

| 1978-10-28 | 316000 | |

| 1978-11-04 | 317000 | |

| 1978-11-11 | 304000 | |

| 1978-11-18 | 342000 | |

| 1978-11-25 | 359000 | |

| 1978-12-02 | 377000 | |

| 1978-12-09 | 344000 | |

| 1978-12-16 | 347000 | |

| 1978-12-23 | 352000 | |

| 1978-12-30 | 358000 | |

| 1979-01-06 | 359000 | |

| 1979-01-13 | 392000 | |

| 1979-01-20 | 337000 | |

| 1979-01-27 | 342000 | |

| 1979-02-03 | 348000 | |

| 1979-02-10 | 359000 | |

| 1979-02-17 | 367000 | |

| 1979-02-24 | 360000 | |

| 1979-03-03 | 355000 | |

| 1979-03-10 | 363000 | |

| 1979-03-17 | 359000 | |

| 1979-03-24 | 353000 | |

| 1979-03-31 | 360000 | |

| 1979-04-07 | 465000 | |

| 1979-04-14 | 457000 | |

| 1979-04-21 | 383000 | |

| 1979-04-28 | 357000 | |

| 1979-05-05 | 353000 | |

| 1979-05-12 | 344000 | |

| 1979-05-19 | 346000 | |

| 1979-05-26 | 349000 | |

| 1979-06-02 | 336000 | |

| 1979-06-09 | 365000 | |

| 1979-06-16 | 351000 | |

| 1979-06-23 | 379000 | |

| 1979-06-30 | 369000 | |

| 1979-07-07 | 368000 | |

| 1979-07-14 | 368000 | |

| 1979-07-21 | 395000 | |

| 1979-07-28 | 386000 | |

| 1979-08-04 | 412000 | |

| 1979-08-11 | 386000 | |

| 1979-08-18 | 387000 | |

| 1979-08-25 | 390000 | |

| 1979-09-01 | 389000 | |

| 1979-09-08 | 378000 | |

| 1979-09-15 | 384000 | |

| 1979-09-22 | 388000 | |

| 1979-09-29 | 390000 | |

| 1979-10-06 | 412000 | |

| 1979-10-13 | 393000 | |

| 1979-10-20 | 406000 | |

| 1979-10-27 | 398000 | |

| 1979-11-03 | 395000 | |

| 1979-11-10 | 414000 | |

| 1979-11-17 | 430000 | |

| 1979-11-24 | 414000 | |

| 1979-12-01 | 416000 | |

| 1979-12-08 | 415000 | |

| 1979-12-15 | 411000 | |

| 1979-12-22 | 471000 | |

| 1979-12-29 | 428000 | |

| 1980-01-05 | 394000 | |

| 1980-01-12 | 405000 | |

| 1980-01-19 | 446000 | |

| 1980-01-26 | 412000 | |

| 1980-02-02 | 404000 | |

| 1980-02-09 | 425000 | |

| 1980-02-16 | 415000 | |

| 1980-02-23 | 428000 | |

| 1980-03-01 | 409000 | |

| 1980-03-08 | 418000 | |

| 1980-03-15 | 432000 | |

| 1980-03-22 | 435000 | |

| 1980-03-29 | 475000 | |

| 1980-04-05 | 464000 | |

| 1980-04-12 | 544000 | |

| 1980-04-19 | 548000 | |

| 1980-04-26 | 563000 | |

| 1980-05-03 | 572000 | |

| 1980-05-10 | 601000 | |

| 1980-05-17 | 642000 | |

| 1980-05-24 | 627000 | |

| 1980-05-31 | 637000 | |

| 1980-06-07 | 610000 | |

| 1980-06-14 | 592000 | |

| 1980-06-21 | 599000 | |

| 1980-06-28 | 627000 | |

| 1980-07-05 | 579000 | |

| 1980-07-12 | 533000 | |

| 1980-07-19 | 567000 | |

| 1980-07-26 | 558000 | |

| 1980-08-02 | 569000 | |

| 1980-08-09 | 533000 | |

| 1980-08-16 | 525000 | |

| 1980-08-23 | 512000 | |

| 1980-08-30 | 502000 | |

| 1980-09-06 | 511000 | |

| 1980-09-13 | 492000 | |

| 1980-09-20 | 465000 | |

| 1980-09-27 | 463000 | |

| 1980-10-04 | 462000 | |

| 1980-10-11 | 447000 | |

| 1980-10-18 | 425000 | |

| 1980-10-25 | 418000 | |

| 1980-11-01 | 419000 | |

| 1980-11-08 | 407000 | |

| 1980-11-15 | 427000 | |

| 1980-11-22 | 398000 | |

| 1980-11-29 | 412000 | |

| 1980-12-06 | 416000 | |

| 1980-12-13 | 413000 | |

| 1980-12-20 | 412000 | |

| 1980-12-27 | 399000 | |

| 1981-01-03 | 410000 | |

| 1981-01-10 | 419000 | |

| 1981-01-17 | 421000 | |

| 1981-01-24 | 396000 | |

| 1981-01-31 | 419000 | |

| 1981-02-07 | 420000 | |

| 1981-02-14 | 423000 | |

| 1981-02-21 | 438000 | |

| 1981-02-28 | 434000 | |

| 1981-03-07 | 409000 | |

| 1981-03-14 | 408000 | |

| 1981-03-21 | 401000 | |

| 1981-03-28 | 412000 | |

| 1981-04-04 | 417000 | |

| 1981-04-11 | 396000 | |

| 1981-04-18 | 392000 | |

| 1981-04-25 | 436000 | |

| 1981-05-02 | 413000 | |

| 1981-05-09 | 423000 | |

| 1981-05-16 | 414000 | |

| 1981-05-23 | 415000 | |

| 1981-05-30 | 417000 | |

| 1981-06-06 | 428000 | |

| 1981-06-13 | 425000 | |

| 1981-06-20 | 435000 | |

| 1981-06-27 | 444000 | |

| 1981-07-04 | 460000 | |

| 1981-07-11 | 426000 | |

| 1981-07-18 | 430000 | |

| 1981-07-25 | 407000 | |

| 1981-08-01 | 476000 | |

| 1981-08-08 | 448000 | |

| 1981-08-15 | 442000 | |

| 1981-08-22 | 434000 | |

| 1981-08-29 | 451000 | |

| 1981-09-05 | 473000 | |

| 1981-09-12 | 454000 | |

| 1981-09-19 | 475000 | |

| 1981-09-26 | 491000 | |

| 1981-10-03 | 489000 | |

| 1981-10-10 | 491000 | |

| 1981-10-17 | 487000 | |

| 1981-10-24 | 483000 | |

| 1981-10-31 | 514000 | |

| 1981-11-07 | 514000 | |

| 1981-11-14 | 517000 | |

| 1981-11-21 | 464000 | |

| 1981-11-28 | 552000 | |

| 1981-12-05 | 558000 | |

| 1981-12-12 | 551000 | |

| 1981-12-19 | 539000 | |

| 1981-12-26 | 556000 | |

| 1982-01-02 | 495000 | |

| 1982-01-09 | 545000 | |

| 1982-01-16 | 489000 | |

| 1982-01-23 | 564000 | |

| 1982-01-30 | 583000 | |

| 1982-02-06 | 556000 | |

| 1982-02-13 | 507000 | |

| 1982-02-20 | 544000 | |

| 1982-02-27 | 528000 | |

| 1982-03-06 | 556000 | |

| 1982-03-13 | 539000 | |

| 1982-03-20 | 557000 | |

| 1982-03-27 | 574000 | |

| 1982-04-03 | 578000 | |

| 1982-04-10 | 585000 | |

| 1982-04-17 | 597000 | |

| 1982-04-24 | 588000 | |

| 1982-05-01 | 576000 | |

| 1982-05-08 | 584000 | |

| 1982-05-15 | 585000 | |

| 1982-05-22 | 586000 | |

| 1982-05-29 | 588000 | |

| 1982-06-05 | 611000 | |

| 1982-06-12 | 614000 | |

| 1982-06-19 | 591000 | |

| 1982-06-26 | 582000 | |

| 1982-07-03 | 600000 | |

| 1982-07-10 | 572000 | |

| 1982-07-17 | 567000 | |

| 1982-07-24 | 536000 | |

| 1982-07-31 | 605000 | |

| 1982-08-07 | 606000 | |

| 1982-08-14 | 637000 | |

| 1982-08-21 | 628000 | |

| 1982-08-28 | 647000 | |

| 1982-09-04 | 651000 | |

| 1982-09-11 | 641000 | |

| 1982-09-18 | 680000 | |

| 1982-09-25 | 671000 | |

| 1982-10-02 | 695000 | |

| 1982-10-09 | 651000 | |

| 1982-10-16 | 656000 | |

| 1982-10-23 | 623000 | |

| 1982-10-30 | 637000 | |

| 1982-11-06 | 589000 | |

| 1982-11-13 | 599000 | |

| 1982-11-20 | 577000 | |

| 1982-11-27 | 612000 | |

| 1982-12-04 | 557000 | |

| 1982-12-11 | 533000 | |

| 1982-12-18 | 516000 | |

| 1982-12-25 | 489000 | |

| 1983-01-01 | 534000 | |

| 1983-01-08 | 510000 | |

| 1983-01-15 | 479000 | |

| 1983-01-22 | 479000 | |

| 1983-01-29 | 503000 | |

| 1983-02-05 | 501000 | |

| 1983-02-12 | 486000 | |

| 1983-02-19 | 487000 | |

| 1983-02-26 | 481000 | |

| 1983-03-05 | 495000 | |

| 1983-03-12 | 475000 | |

| 1983-03-19 | 470000 | |

| 1983-03-26 | 481000 | |

| 1983-04-02 | 491000 | |

| 1983-04-09 | 496000 | |

| 1983-04-16 | 515000 | |

| 1983-04-23 | 488000 | |

| 1983-04-30 | 490000 | |

| 1983-05-07 | 494000 | |

| 1983-05-14 | 464000 | |

| 1983-05-21 | 460000 | |

| 1983-05-28 | 454000 | |

| 1983-06-04 | 459000 | |

| 1983-06-11 | 442000 | |

| 1983-06-18 | 434000 | |

| 1983-06-25 | 442000 | |

| 1983-07-02 | 422000 | |

| 1983-07-09 | 412000 | |

| 1983-07-16 | 396000 | |

| 1983-07-23 | 395000 | |

| 1983-07-30 | 415000 | |

| 1983-08-06 | 415000 | |

| 1983-08-13 | 457000 | |

| 1983-08-20 | 445000 | |

| 1983-08-27 | 426000 | |

| 1983-09-03 | 411000 | |

| 1983-09-10 | 403000 | |

| 1983-09-17 | 405000 | |

| 1983-09-24 | 416000 | |

| 1983-10-01 | 413000 | |

| 1983-10-08 | 406000 | |

| 1983-10-15 | 394000 | |

| 1983-10-22 | 394000 | |

| 1983-10-29 | 404000 | |

| 1983-11-05 | 395000 | |

| 1983-11-12 | 390000 | |

| 1983-11-19 | 387000 | |

| 1983-11-26 | 398000 | |

| 1983-12-03 | 365000 | |

| 1983-12-10 | 368000 | |

| 1983-12-17 | 362000 | |

| 1983-12-24 | 377000 | |

| 1983-12-31 | 372000 | |

| 1984-01-07 | 356000 | |

| 1984-01-14 | 351000 | |

| 1984-01-21 | 333000 | |

| 1984-01-28 | 364000 | |

| 1984-02-04 | 342000 | |

| 1984-02-11 | 338000 | |

| 1984-02-18 | 334000 | |

| 1984-02-25 | 343000 | |

| 1984-03-03 | 347000 | |

| 1984-03-10 | 346000 | |

| 1984-03-17 | 349000 | |

| 1984-03-24 | 346000 | |

| 1984-03-31 | 341000 | |

| 1984-04-07 | 381000 | |

| 1984-04-14 | 357000 | |

| 1984-04-21 | 364000 | |

| 1984-04-28 | 375000 | |

| 1984-05-05 | 365000 | |

| 1984-05-12 | 368000 | |

| 1984-05-19 | 354000 | |

| 1984-05-26 | 354000 | |

| 1984-06-02 | 355000 | |

| 1984-06-09 | 369000 | |

| 1984-06-16 | 361000 | |

| 1984-06-23 | 362000 | |

| 1984-06-30 | 360000 | |

| 1984-07-07 | 366000 | |

| 1984-07-14 | 360000 | |

| 1984-07-21 | 357000 | |

| 1984-07-28 | 359000 | |

| 1984-08-04 | 382000 | |

| 1984-08-11 | 380000 | |

| 1984-08-18 | 401000 | |

| 1984-08-25 | 395000 | |

| 1984-09-01 | 385000 | |

| 1984-09-08 | 402000 | |

| 1984-09-15 | 393000 | |

| 1984-09-22 | 395000 | |

| 1984-09-29 | 402000 | |

| 1984-10-06 | 403000 | |

| 1984-10-13 | 410000 | |

| 1984-10-20 | 439000 | |

| 1984-10-27 | 425000 | |

| 1984-11-03 | 423000 | |

| 1984-11-10 | 393000 | |

| 1984-11-17 | 383000 | |

| 1984-11-24 | 429000 | |

| 1984-12-01 | 401000 | |

| 1984-12-08 | 383000 | |

| 1984-12-15 | 386000 | |

| 1984-12-22 | 379000 | |

| 1984-12-29 | 379000 | |

| 1985-01-05 | 369000 | |

| 1985-01-12 | 387000 | |

| 1985-01-19 | 359000 | |

| 1985-01-26 | 368000 | |

| 1985-02-02 | 386000 | |

| 1985-02-09 | 401000 | |

| 1985-02-16 | 390000 | |

| 1985-02-23 | 390000 | |

| 1985-03-02 | 374000 | |

| 1985-03-09 | 385000 | |

| 1985-03-16 | 386000 | |

| 1985-03-23 | 373000 | |

| 1985-03-30 | 386000 | |

| 1985-04-06 | 405000 | |

| 1985-04-13 | 411000 | |

| 1985-04-20 | 391000 | |

| 1985-04-27 | 386000 | |

| 1985-05-04 | 390000 | |

| 1985-05-11 | 394000 | |

| 1985-05-18 | 391000 | |

| 1985-05-25 | 396000 | |

| 1985-06-01 | 393000 | |

| 1985-06-08 | 403000 | |

| 1985-06-15 | 390000 | |

| 1985-06-22 | 386000 | |

| 1985-06-29 | 390000 | |

| 1985-07-06 | 395000 | |

| 1985-07-13 | 386000 | |

| 1985-07-20 | 370000 | |

| 1985-07-27 | 362000 | |

| 1985-08-03 | 407000 | |

| 1985-08-10 | 402000 | |

| 1985-08-17 | 399000 | |

| 1985-08-24 | 405000 | |

| 1985-08-31 | 409000 | |

| 1985-09-07 | 426000 | |

| 1985-09-14 | 408000 | |

| 1985-09-21 | 401000 | |

| 1985-09-28 | 399000 | |

| 1985-10-05 | 405000 | |

| 1985-10-12 | 400000 | |

| 1985-10-19 | 400000 | |

| 1985-10-26 | 418000 | |

| 1985-11-02 | 398000 | |

| 1985-11-09 | 397000 | |

| 1985-11-16 | 397000 | |

| 1985-11-23 | 382000 | |

| 1985-11-30 | 393000 | |

| 1985-12-07 | 399000 | |

| 1985-12-14 | 382000 | |

| 1985-12-21 | 370000 | |

| 1985-12-28 | 390000 | |

| 1986-01-04 | 362000 | |

| 1986-01-11 | 397000 | |

| 1986-01-18 | 364000 | |

| 1986-01-25 | 344000 | |

| 1986-02-01 | 364000 | |

| 1986-02-08 | 366000 | |

| 1986-02-15 | 358000 | |

| 1986-02-22 | 390000 | |

| 1986-03-01 | 375000 | |

| 1986-03-08 | 366000 | |

| 1986-03-15 | 382000 | |

| 1986-03-22 | 387000 | |

| 1986-03-29 | 396000 | |

| 1986-04-05 | 381000 | |

| 1986-04-12 | 388000 | |

| 1986-04-19 | 383000 | |

| 1986-04-26 | 391000 | |

| 1986-05-03 | 392000 | |

| 1986-05-10 | 395000 | |

| 1986-05-17 | 384000 | |

| 1986-05-24 | 386000 | |

| 1986-05-31 | 373000 | |

| 1986-06-07 | 375000 | |

| 1986-06-14 | 369000 | |

| 1986-06-21 | 367000 | |

| 1986-06-28 | 371000 | |

| 1986-07-05 | 371000 | |

| 1986-07-12 | 361000 | |

| 1986-07-19 | 354000 | |

| 1986-07-26 | 362000 | |

| 1986-08-02 | 416000 | |

| 1986-08-09 | 416000 | |

| 1986-08-16 | 407000 | |

| 1986-08-23 | 397000 | |

| 1986-08-30 | 401000 | |

| 1986-09-06 | 400000 | |

| 1986-09-13 | 394000 | |

| 1986-09-20 | 399000 | |

| 1986-09-27 | 389000 | |

| 1986-10-04 | 391000 | |

| 1986-10-11 | 387000 | |

| 1986-10-18 | 385000 | |

| 1986-10-25 | 370000 | |

| 1986-11-01 | 364000 | |

| 1986-11-08 | 349000 | |

| 1986-11-15 | 368000 | |

| 1986-11-22 | 369000 | |

| 1986-11-29 | 366000 | |

| 1986-12-06 | 363000 | |

| 1986-12-13 | 375000 | |

| 1986-12-20 | 350000 | |

| 1986-12-27 | 345000 | |

| 1987-01-03 | 323000 | |

| 1987-01-10 | 348000 | |

| 1987-01-17 | 341000 | |

| 1987-01-24 | 346000 | |

| 1987-01-31 | 370000 | |

| 1987-02-07 | 368000 | |

| 1987-02-14 | 338000 | |

| 1987-02-21 | 341000 | |

| 1987-02-28 | 348000 | |

| 1987-03-07 | 337000 | |

| 1987-03-14 | 335000 | |

| 1987-03-21 | 335000 | |

| 1987-03-28 | 326000 | |

| 1987-04-04 | 330000 | |

| 1987-04-11 | 338000 | |

| 1987-04-18 | 349000 | |

| 1987-04-25 | 328000 | |

| 1987-05-02 | 330000 | |

| 1987-05-09 | 315000 | |

| 1987-05-16 | 341000 | |

| 1987-05-23 | 343000 | |

| 1987-05-30 | 326000 | |

| 1987-06-06 | 328000 | |

| 1987-06-13 | 316000 | |

| 1987-06-20 | 319000 | |

| 1987-06-27 | 326000 | |

| 1987-07-04 | 326000 | |

| 1987-07-11 | 317000 | |

| 1987-07-18 | 310000 | |

| 1987-07-25 | 324000 | |

| 1987-08-01 | 348000 | |

| 1987-08-08 | 327000 | |

| 1987-08-15 | 319000 | |

| 1987-08-22 | 312000 | |

| 1987-08-29 | 322000 | |

| 1987-09-05 | 316000 | |

| 1987-09-12 | 297000 | |

| 1987-09-19 | 309000 | |

| 1987-09-26 | 317000 | |

| 1987-10-03 | 301000 | |

| 1987-10-10 | 308000 | |

| 1987-10-17 | 301000 | |

| 1987-10-24 | 301000 | |

| 1987-10-31 | 289000 | |

| 1987-11-07 | 297000 | |

| 1987-11-14 | 307000 | |

| 1987-11-21 | 317000 | |

| 1987-11-28 | 306000 | |

| 1987-12-05 | 319000 | |

| 1987-12-12 | 317000 | |

| 1987-12-19 | 323000 | |

| 1987-12-26 | 316000 | |

| 1988-01-02 | 315000 | |

| 1988-01-09 | 325000 | |

| 1988-01-16 | 361000 | |

| 1988-01-23 | 335000 | |

| 1988-01-30 | 342000 | |

| 1988-02-06 | 318000 | |

| 1988-02-13 | 311000 | |

| 1988-02-20 | 327000 | |

| 1988-02-27 | 319000 | |

| 1988-03-05 | 307000 | |

| 1988-03-12 | 304000 | |

| 1988-03-19 | 307000 | |

| 1988-03-26 | 304000 | |

| 1988-04-02 | 309000 | |

| 1988-04-09 | 313000 | |

| 1988-04-16 | 314000 | |

| 1988-04-23 | 312000 | |

| 1988-04-30 | 313000 | |

| 1988-05-07 | 309000 | |

| 1988-05-14 | 314000 | |

| 1988-05-21 | 319000 | |

| 1988-05-28 | 313000 | |

| 1988-06-04 | 310000 | |

| 1988-06-11 | 305000 | |

| 1988-06-18 | 311000 | |

| 1988-06-25 | 307000 | |

| 1988-07-02 | 305000 | |

| 1988-07-09 | 303000 | |

| 1988-07-16 | 315000 | |

| 1988-07-23 | 354000 | |

| 1988-07-30 | 331000 | |

| 1988-08-06 | 316000 | |

| 1988-08-13 | 312000 | |

| 1988-08-20 | 316000 | |

| 1988-08-27 | 315000 | |

| 1988-09-03 | 306000 | |

| 1988-09-10 | 305000 | |

| 1988-09-17 | 306000 | |

| 1988-09-24 | 301000 | |

| 1988-10-01 | 292000 | |

| 1988-10-08 | 292000 | |

| 1988-10-15 | 293000 | |

| 1988-10-22 | 286000 | |

| 1988-10-29 | 294000 | |

| 1988-11-05 | 285000 | |

| 1988-11-12 | 284000 | |

| 1988-11-19 | 294000 | |

| 1988-11-26 | 299000 | |

| 1988-12-03 | 298000 | |

| 1988-12-10 | 285000 | |

| 1988-12-17 | 293000 | |

| 1988-12-24 | 286000 | |

| 1988-12-31 | 304000 | |

| 1989-01-07 | 299000 | |

| 1989-01-14 | 283000 | |

| 1989-01-21 | 282000 | |

| 1989-01-28 | 295000 | |

| 1989-02-04 | 288000 | |

| 1989-02-11 | 322000 | |

| 1989-02-18 | 305000 | |

| 1989-02-25 | 300000 | |

| 1989-03-04 | 325000 | |

| 1989-03-11 | 325000 | |

| 1989-03-18 | 319000 | |

| 1989-03-25 | 319000 | |

| 1989-04-01 | 323000 | |

| 1989-04-08 | 314000 | |

| 1989-04-15 | 307000 | |

| 1989-04-22 | 304000 | |

| 1989-04-29 | 311000 | |

| 1989-05-06 | 320000 | |

| 1989-05-13 | 332000 | |

| 1989-05-20 | 321000 | |

| 1989-05-27 | 325000 | |

| 1989-06-03 | 325000 | |

| 1989-06-10 | 332000 | |

| 1989-06-17 | 337000 | |

| 1989-06-24 | 338000 | |

| 1989-07-01 | 349000 | |

| 1989-07-08 | 341000 | |

| 1989-07-15 | 349000 | |

| 1989-07-22 | 332000 | |

| 1989-07-29 | 337000 | |

| 1989-08-05 | 338000 | |

| 1989-08-12 | 341000 | |

| 1989-08-19 | 327000 | |

| 1989-08-26 | 332000 | |

| 1989-09-02 | 329000 | |

| 1989-09-09 | 336000 | |

| 1989-09-16 | 334000 | |

| 1989-09-23 | 334000 | |

| 1989-09-30 | 347000 | |

| 1989-10-07 | 407000 | |

| 1989-10-14 | 345000 | |

| 1989-10-21 | 347000 | |

| 1989-10-28 | 354000 | |

| 1989-11-04 | 333000 | |

| 1989-11-11 | 336000 | |

| 1989-11-18 | 336000 | |

| 1989-11-25 | 342000 | |

| 1989-12-02 | 344000 | |

| 1989-12-09 | 338000 | |

| 1989-12-16 | 355000 | |

| 1989-12-23 | 381000 | |

| 1989-12-30 | 358000 | |

| 1990-01-06 | 355000 | |

| 1990-01-13 | 369000 | |

| 1990-01-20 | 375000 | |

| 1990-01-27 | 345000 | |

| 1990-02-03 | 368000 | |

| 1990-02-10 | 367000 | |

| 1990-02-17 | 348000 | |

| 1990-02-24 | 350000 | |

| 1990-03-03 | 351000 | |

| 1990-03-10 | 349000 | |

| 1990-03-17 | 349000 | |

| 1990-03-24 | 331000 | |

| 1990-03-31 | 346000 | |

| 1990-04-07 | 367000 | |

| 1990-04-14 | 357000 | |

| 1990-04-21 | 360000 | |

| 1990-04-28 | 363000 | |

| 1990-05-05 | 354000 | |

| 1990-05-12 | 355000 | |

| 1990-05-19 | 353000 | |

| 1990-05-26 | 359000 | |

| 1990-06-02 | 368000 | |

| 1990-06-09 | 359000 | |

| 1990-06-16 | 359000 | |

| 1990-06-23 | 362000 | |

| 1990-06-30 | 364000 | |

| 1990-07-07 | 362000 | |

| 1990-07-14 | 367000 | |

| 1990-07-21 | 370000 | |

| 1990-07-28 | 369000 | |

| 1990-08-04 | 369000 | |

| 1990-08-11 | 381000 | |

| 1990-08-18 | 393000 | |

| 1990-08-25 | 394000 | |

| 1990-09-01 | 392000 | |

| 1990-09-08 | 390000 | |

| 1990-09-15 | 395000 | |

| 1990-09-22 | 389000 | |

| 1990-09-29 | 404000 | |

| 1990-10-06 | 404000 | |

| 1990-10-13 | 422000 | |

| 1990-10-20 | 435000 | |

| 1990-10-27 | 440000 | |

| 1990-11-03 | 430000 | |

| 1990-11-10 | 448000 | |

| 1990-11-17 | 447000 | |

| 1990-11-24 | 462000 | |

| 1990-12-01 | 451000 | |

| 1990-12-08 | 449000 | |

| 1990-12-15 | 447000 | |

| 1990-12-22 | 474000 | |

| 1990-12-29 | 454000 | |

| 1991-01-05 | 415000 | |

| 1991-01-12 | 437000 | |

| 1991-01-19 | 445000 | |

| 1991-01-26 | 462000 | |

| 1991-02-02 | 483000 | |

| 1991-02-09 | 480000 | |

| 1991-02-16 | 474000 | |

| 1991-02-23 | 499000 | |

| 1991-03-02 | 488000 | |

| 1991-03-09 | 499000 | |

| 1991-03-16 | 498000 | |

| 1991-03-23 | 509000 | |

| 1991-03-30 | 499000 | |

| 1991-04-06 | 452000 | |

| 1991-04-13 | 477000 | |

| 1991-04-20 | 478000 | |

| 1991-04-27 | 462000 | |

| 1991-05-04 | 451000 | |

| 1991-05-11 | 446000 | |

| 1991-05-18 | 448000 | |

| 1991-05-25 | 443000 | |

| 1991-06-01 | 432000 | |

| 1991-06-08 | 441000 | |

| 1991-06-15 | 429000 | |

| 1991-06-22 | 423000 | |

| 1991-06-29 | 418000 | |

| 1991-07-06 | 422000 | |

| 1991-07-13 | 420000 | |

| 1991-07-20 | 408000 | |

| 1991-07-27 | 423000 | |

| 1991-08-03 | 438000 | |

| 1991-08-10 | 437000 | |

| 1991-08-17 | 433000 | |

| 1991-08-24 | 425000 | |

| 1991-08-31 | 425000 | |

| 1991-09-07 | 424000 | |

| 1991-09-14 | 418000 | |

| 1991-09-21 | 419000 | |

| 1991-09-28 | 437000 | |

| 1991-10-05 | 424000 | |

| 1991-10-12 | 425000 | |

| 1991-10-19 | 419000 | |

| 1991-10-26 | 423000 | |

| 1991-11-02 | 447000 | |

| 1991-11-09 | 453000 | |

| 1991-11-16 | 439000 | |

| 1991-11-23 | 444000 | |

| 1991-11-30 | 444000 | |

| 1991-12-07 | 475000 | |

| 1991-12-14 | 475000 | |

| 1991-12-21 | 436000 | |

| 1991-12-28 | 441000 | |

| 1992-01-04 | 432000 | |

| 1992-01-11 | 440000 | |

| 1992-01-18 | 443000 | |

| 1992-01-25 | 441000 | |

| 1992-02-01 | 440000 | |

| 1992-02-08 | 445000 | |

| 1992-02-15 | 446000 | |

| 1992-02-22 | 436000 | |

| 1992-02-29 | 444000 | |

| 1992-03-07 | 421000 | |

| 1992-03-14 | 437000 | |

| 1992-03-21 | 440000 | |

| 1992-03-28 | 420000 | |

| 1992-04-04 | 412000 | |

| 1992-04-11 | 413000 | |

| 1992-04-18 | 424000 | |

| 1992-04-25 | 424000 | |

| 1992-05-02 | 431000 | |

| 1992-05-09 | 417000 | |

| 1992-05-16 | 414000 | |

| 1992-05-23 | 414000 | |

| 1992-05-30 | 411000 | |

| 1992-06-06 | 416000 | |

| 1992-06-13 | 420000 | |

| 1992-06-20 | 419000 | |

| 1992-06-27 | 420000 | |

| 1992-07-04 | 407000 | |

| 1992-07-11 | 408000 | |

| 1992-07-18 | 392000 | |

| 1992-07-25 | 564000 | |

| 1992-08-01 | 423000 | |

| 1992-08-08 | 406000 | |

| 1992-08-15 | 401000 | |

| 1992-08-22 | 398000 | |

| 1992-08-29 | 408000 | |

| 1992-09-05 | 416000 | |

| 1992-09-12 | 416000 | |

| 1992-09-19 | 427000 | |

| 1992-09-26 | 409000 | |

| 1992-10-03 | 398000 | |

| 1992-10-10 | 374000 | |

| 1992-10-17 | 385000 | |

| 1992-10-24 | 367000 | |

| 1992-10-31 | 365000 | |

| 1992-11-07 | 374000 | |

| 1992-11-14 | 377000 | |

| 1992-11-21 | 357000 | |

| 1992-11-28 | 341000 | |

| 1992-12-05 | 350000 | |

| 1992-12-12 | 359000 | |

| 1992-12-19 | 334000 | |

| 1992-12-26 | 313000 | |

| 1993-01-02 | 341000 | |

| 1993-01-09 | 354000 | |

| 1993-01-16 | 352000 | |

| 1993-01-23 | 341000 | |

| 1993-01-30 | 340000 | |

| 1993-02-06 | 319000 | |

| 1993-02-13 | 321000 | |

| 1993-02-20 | 351000 | |

| 1993-02-27 | 362000 | |

| 1993-03-06 | 354000 | |

| 1993-03-13 | 346000 | |

| 1993-03-20 | 338000 | |

| 1993-03-27 | 366000 | |

| 1993-04-03 | 365000 | |

| 1993-04-10 | 353000 | |

| 1993-04-17 | 351000 | |

| 1993-04-24 | 350000 | |

| 1993-05-01 | 343000 | |

| 1993-05-08 | 339000 | |

| 1993-05-15 | 345000 | |

| 1993-05-22 | 342000 | |

| 1993-05-29 | 349000 | |

| 1993-06-05 | 343000 | |

| 1993-06-12 | 343000 | |

| 1993-06-19 | 345000 | |

| 1993-06-26 | 340000 | |

| 1993-07-03 | 334000 | |

| 1993-07-10 | 314000 | |

| 1993-07-17 | 335000 | |

| 1993-07-24 | 415000 | |

| 1993-07-31 | 356000 | |

| 1993-08-07 | 346000 | |

| 1993-08-14 | 339000 | |

| 1993-08-21 | 342000 | |

| 1993-08-28 | 337000 | |

| 1993-09-04 | 334000 | |

| 1993-09-11 | 333000 | |

| 1993-09-18 | 346000 | |

| 1993-09-25 | 343000 | |

| 1993-10-02 | 333000 | |

| 1993-10-09 | 355000 | |

| 1993-10-16 | 359000 | |

| 1993-10-23 | 354000 | |

| 1993-10-30 | 348000 | |

| 1993-11-06 | 350000 | |

| 1993-11-13 | 341000 | |

| 1993-11-20 | 336000 | |

| 1993-11-27 | 337000 | |

| 1993-12-04 | 337000 | |

| 1993-12-11 | 334000 | |

| 1993-12-18 | 331000 | |

| 1993-12-25 | 290000 | |

| 1994-01-01 | 341000 | |

| 1994-01-08 | 343000 | |

| 1994-01-15 | 355000 | |

| 1994-01-22 | 351000 | |

| 1994-01-29 | 406000 | |

| 1994-02-05 | 361000 | |

| 1994-02-12 | 354000 | |

| 1994-02-19 | 352000 | |

| 1994-02-26 | 327000 | |

| 1994-03-05 | 348000 | |

| 1994-03-12 | 341000 | |

| 1994-03-19 | 332000 | |

| 1994-03-26 | 322000 | |

| 1994-04-02 | 342000 | |

| 1994-04-09 | 349000 | |

| 1994-04-16 | 354000 | |

| 1994-04-23 | 331000 | |

| 1994-04-30 | 344000 | |

| 1994-05-07 | 371000 | |

| 1994-05-14 | 360000 | |

| 1994-05-21 | 357000 | |

| 1994-05-28 | 348000 | |

| 1994-06-04 | 345000 | |

| 1994-06-11 | 338000 | |

| 1994-06-18 | 336000 | |

| 1994-06-25 | 341000 | |

| 1994-07-02 | 334000 | |

| 1994-07-09 | 341000 | |

| 1994-07-16 | 359000 | |

| 1994-07-23 | 345000 | |

| 1994-07-30 | 332000 | |

| 1994-08-06 | 338000 | |

| 1994-08-13 | 335000 | |

| 1994-08-20 | 331000 | |

| 1994-08-27 | 341000 | |

| 1994-09-03 | 339000 | |

| 1994-09-10 | 331000 | |

| 1994-09-17 | 326000 | |

| 1994-09-24 | 325000 | |

| 1994-10-01 | 330000 | |

| 1994-10-08 | 341000 | |

| 1994-10-15 | 335000 | |

| 1994-10-22 | 330000 | |

| 1994-10-29 | 331000 | |

| 1994-11-05 | 328000 | |

| 1994-11-12 | 329000 | |

| 1994-11-19 | 326000 | |

| 1994-11-26 | 329000 | |

| 1994-12-03 | 324000 | |

| 1994-12-10 | 329000 | |

| 1994-12-17 | 330000 | |

| 1994-12-24 | 314000 | |

| 1994-12-31 | 319000 | |

| 1995-01-07 | 338000 | |

| 1995-01-14 | 347000 | |

| 1995-01-21 | 325000 | |

| 1995-01-28 | 324000 | |

| 1995-02-04 | 324000 | |

| 1995-02-11 | 348000 | |

| 1995-02-18 | 343000 | |

| 1995-02-25 | 336000 | |

| 1995-03-04 | 339000 | |

| 1995-03-11 | 347000 | |

| 1995-03-18 | 343000 | |

| 1995-03-25 | 332000 | |

| 1995-04-01 | 335000 | |

| 1995-04-08 | 347000 | |

| 1995-04-15 | 355000 | |

| 1995-04-22 | 349000 | |

| 1995-04-29 | 365000 | |

| 1995-05-06 | 364000 | |

| 1995-05-13 | 366000 | |

| 1995-05-20 | 377000 | |

| 1995-05-27 | 374000 | |

| 1995-06-03 | 362000 | |

| 1995-06-10 | 367000 | |

| 1995-06-17 | 378000 | |

| 1995-06-24 | 358000 | |

| 1995-07-01 | 355000 | |

| 1995-07-08 | 372000 | |

| 1995-07-15 | 389000 | |

| 1995-07-22 | 390000 | |

| 1995-07-29 | 351000 | |

| 1995-08-05 | 351000 | |

| 1995-08-12 | 353000 | |

| 1995-08-19 | 362000 | |

| 1995-08-26 | 359000 | |

| 1995-09-02 | 355000 | |

| 1995-09-09 | 371000 | |

| 1995-09-16 | 376000 | |

| 1995-09-23 | 353000 | |

| 1995-09-30 | 355000 | |

| 1995-10-07 | 374000 | |

| 1995-10-14 | 369000 | |

| 1995-10-21 | 366000 | |

| 1995-10-28 | 377000 | |

| 1995-11-04 | 380000 | |

| 1995-11-11 | 370000 | |

| 1995-11-18 | 379000 | |

| 1995-11-25 | 379000 | |

| 1995-12-02 | 373000 | |

| 1995-12-09 | 346000 | |

| 1995-12-16 | 373000 | |

| 1995-12-23 | 374000 | |

| 1995-12-30 | 359000 | |

| 1996-01-06 | 361000 | |

| 1996-01-13 | 333000 | |

| 1996-01-20 | 415000 | |

| 1996-01-27 | 387000 | |

| 1996-02-03 | 374000 | |

| 1996-02-10 | 387000 | |

| 1996-02-17 | 383000 | |

| 1996-02-24 | 365000 | |

| 1996-03-02 | 368000 | |

| 1996-03-09 | 361000 | |

| 1996-03-16 | 384000 | |

| 1996-03-23 | 426000 | |

| 1996-03-30 | 393000 | |

| 1996-04-06 | 369000 | |

| 1996-04-13 | 357000 | |

| 1996-04-20 | 368000 | |

| 1996-04-27 | 343000 | |

| 1996-05-04 | 338000 | |

| 1996-05-11 | 352000 | |

| 1996-05-18 | 345000 | |

| 1996-05-25 | 343000 | |

| 1996-06-01 | 340000 | |

| 1996-06-08 | 351000 | |

| 1996-06-15 | 342000 | |

| 1996-06-22 | 341000 | |

| 1996-06-29 | 337000 | |

| 1996-07-06 | 342000 | |

| 1996-07-13 | 347000 | |

| 1996-07-20 | 332000 | |

| 1996-07-27 | 327000 | |

| 1996-08-03 | 326000 | |

| 1996-08-10 | 331000 | |

| 1996-08-17 | 336000 | |

| 1996-08-24 | 337000 | |

| 1996-08-31 | 329000 | |

| 1996-09-07 | 333000 | |

| 1996-09-14 | 338000 | |

| 1996-09-21 | 352000 | |

| 1996-09-28 | 348000 | |

| 1996-10-05 | 335000 | |

| 1996-10-12 | 334000 | |

| 1996-10-19 | 335000 | |

| 1996-10-26 | 352000 | |

| 1996-11-02 | 334000 | |

| 1996-11-09 | 327000 | |

| 1996-11-16 | 342000 | |

| 1996-11-23 | 347000 | |

| 1996-11-30 | 332000 | |

| 1996-12-07 | 355000 | |

| 1996-12-14 | 352000 | |

| 1996-12-21 | 350000 | |

| 1996-12-28 | 357000 | |

| 1997-01-04 | 347000 | |

| 1997-01-11 | 324000 | |

| 1997-01-18 | 345000 | |

| 1997-01-25 | 340000 | |

| 1997-02-01 | 333000 | |

| 1997-02-08 | 315000 | |

| 1997-02-15 | 313000 | |

| 1997-02-22 | 322000 | |

| 1997-03-01 | 321000 | |

| 1997-03-08 | 317000 | |

| 1997-03-15 | 319000 | |

| 1997-03-22 | 315000 | |

| 1997-03-29 | 325000 | |

| 1997-04-05 | 325000 | |

| 1997-04-12 | 330000 | |

| 1997-04-19 | 316000 | |

| 1997-04-26 | 337000 | |

| 1997-05-03 | 342000 | |

| 1997-05-10 | 318000 | |

| 1997-05-17 | 322000 | |

| 1997-05-24 | 316000 | |

| 1997-05-31 | 321000 | |

| 1997-06-07 | 329000 | |

| 1997-06-14 | 335000 | |

| 1997-06-21 | 316000 | |

| 1997-06-28 | 322000 | |

| 1997-07-05 | 346000 | |

| 1997-07-12 | 328000 | |

| 1997-07-19 | 301000 | |

| 1997-07-26 | 306000 | |

| 1997-08-02 | 320000 | |

| 1997-08-09 | 329000 | |

| 1997-08-16 | 343000 | |

| 1997-08-23 | 327000 | |

| 1997-08-30 | 332000 | |

| 1997-09-06 | 313000 | |

| 1997-09-13 | 314000 | |

| 1997-09-20 | 317000 | |

| 1997-09-27 | 317000 | |

| 1997-10-04 | 311000 | |

| 1997-10-11 | 305000 | |

| 1997-10-18 | 318000 | |

| 1997-10-25 | 306000 | |

| 1997-11-01 | 313000 | |

| 1997-11-08 | 308000 | |

| 1997-11-15 | 325000 | |

| 1997-11-22 | 309000 | |

| 1997-11-29 | 318000 | |

| 1997-12-06 | 317000 | |

| 1997-12-13 | 323000 | |

| 1997-12-20 | 310000 | |

| 1997-12-27 | 303000 | |

| 1998-01-03 | 312000 | |

| 1998-01-10 | 331000 | |

| 1998-01-17 | 341000 | |

| 1998-01-24 | 307000 | |

| 1998-01-31 | 315000 | |

| 1998-02-07 | 311000 | |

| 1998-02-14 | 321000 | |

| 1998-02-21 | 327000 | |

| 1998-02-28 | 317000 | |

| 1998-03-07 | 308000 | |

| 1998-03-14 | 319000 | |

| 1998-03-21 | 321000 | |

| 1998-03-28 | 312000 | |

| 1998-04-04 | 312000 | |

| 1998-04-11 | 304000 | |

| 1998-04-18 | 317000 | |

| 1998-04-25 | 311000 | |

| 1998-05-02 | 304000 | |

| 1998-05-09 | 306000 | |

| 1998-05-16 | 315000 | |

| 1998-05-23 | 309000 | |

| 1998-05-30 | 322000 | |

| 1998-06-06 | 306000 | |

| 1998-06-13 | 321000 | |

| 1998-06-20 | 349000 | |

| 1998-06-27 | 376000 | |

| 1998-07-04 | 362000 | |

| 1998-07-11 | 320000 | |

| 1998-07-18 | 315000 | |

| 1998-07-25 | 335000 | |

| 1998-08-01 | 327000 | |

| 1998-08-08 | 316000 | |

| 1998-08-15 | 308000 | |

| 1998-08-22 | 302000 | |

| 1998-08-29 | 310000 | |

| 1998-09-05 | 313000 | |

| 1998-09-12 | 304000 | |

| 1998-09-19 | 305000 | |

| 1998-09-26 | 294000 | |

| 1998-10-03 | 302000 | |

| 1998-10-10 | 316000 | |

| 1998-10-17 | 318000 | |

| 1998-10-24 | 309000 | |

| 1998-10-31 | 308000 | |

| 1998-11-07 | 316000 | |

| 1998-11-14 | 334000 | |

| 1998-11-21 | 304000 | |

| 1998-11-28 | 310000 | |

| 1998-12-05 | 326000 | |

| 1998-12-12 | 305000 | |

| 1998-12-19 | 297000 | |

| 1998-12-26 | 336000 | |

| 1999-01-02 | 331000 | |

| 1999-01-09 | 345000 | |

| 1999-01-16 | 339000 | |

| 1999-01-23 | 311000 | |

| 1999-01-30 | 305000 | |

| 1999-02-06 | 291000 | |

| 1999-02-13 | 312000 | |

| 1999-02-20 | 302000 | |

| 1999-02-27 | 301000 | |

| 1999-03-06 | 300000 | |

| 1999-03-13 | 308000 | |

| 1999-03-20 | 305000 | |

| 1999-03-27 | 298000 | |

| 1999-04-03 | 310000 | |

| 1999-04-10 | 319000 | |

| 1999-04-17 | 314000 | |

| 1999-04-24 | 291000 | |

| 1999-05-01 | 296000 | |

| 1999-05-08 | 310000 | |

| 1999-05-15 | 301000 | |

| 1999-05-22 | 298000 | |

| 1999-05-29 | 303000 | |

| 1999-06-05 | 303000 | |

| 1999-06-12 | 290000 | |

| 1999-06-19 | 292000 | |

| 1999-06-26 | 291000 | |

| 1999-07-03 | 287000 | |

| 1999-07-10 | 288000 | |

| 1999-07-17 | 309000 | |

| 1999-07-24 | 306000 | |

| 1999-07-31 | 300000 | |

| 1999-08-07 | 295000 | |

| 1999-08-14 | 292000 | |

| 1999-08-21 | 286000 | |

| 1999-08-28 | 290000 | |

| 1999-09-04 | 290000 | |

| 1999-09-11 | 281000 | |

| 1999-09-18 | 281000 | |

| 1999-09-25 | 306000 | |

| 1999-10-02 | 309000 | |

| 1999-10-09 | 291000 | |

| 1999-10-16 | 287000 | |

| 1999-10-23 | 280000 | |

| 1999-10-30 | 285000 | |

| 1999-11-06 | 282000 | |

| 1999-11-13 | 281000 | |

| 1999-11-20 | 276000 | |

| 1999-11-27 | 288000 | |

| 1999-12-04 | 287000 | |

| 1999-12-11 | 272000 | |

| 1999-12-18 | 287000 | |

| 1999-12-25 | 268000 | |

| 2000-01-01 | 286000 | |

| 2000-01-08 | 298000 | |

| 2000-01-15 | 289000 | |

| 2000-01-22 | 284000 | |

| 2000-01-29 | 285000 | |

| 2000-02-05 | 312000 | |

| 2000-02-12 | 300000 | |

| 2000-02-19 | 283000 | |

| 2000-02-26 | 280000 | |

| 2000-03-04 | 286000 | |

| 2000-03-11 | 270000 | |

| 2000-03-18 | 271000 | |

| 2000-03-25 | 272000 | |

| 2000-04-01 | 266000 | |

| 2000-04-08 | 268000 | |

| 2000-04-15 | 259000 | |

| 2000-04-22 | 274000 | |

| 2000-04-29 | 291000 | |

| 2000-05-06 | 293000 | |

| 2000-05-13 | 276000 | |

| 2000-05-20 | 280000 | |

| 2000-05-27 | 280000 | |

| 2000-06-03 | 290000 | |

| 2000-06-10 | 284000 | |

| 2000-06-17 | 294000 | |

| 2000-06-24 | 296000 | |

| 2000-07-01 | 281000 | |

| 2000-07-08 | 293000 | |

| 2000-07-15 | 303000 | |

| 2000-07-22 | 300000 | |

| 2000-07-29 | 298000 | |

| 2000-08-05 | 306000 | |

| 2000-08-12 | 315000 | |

| 2000-08-19 | 318000 | |

| 2000-08-26 | 312000 | |

| 2000-09-02 | 301000 | |

| 2000-09-09 | 309000 | |

| 2000-09-16 | 311000 | |

| 2000-09-23 | 288000 | |

| 2000-09-30 | 292000 | |

| 2000-10-07 | 309000 | |

| 2000-10-14 | 299000 | |

| 2000-10-21 | 295000 | |

| 2000-10-28 | 301000 | |

| 2000-11-04 | 331000 | |

| 2000-11-11 | 318000 | |

| 2000-11-18 | 332000 | |

| 2000-11-25 | 356000 | |

| 2000-12-02 | 338000 | |

| 2000-12-09 | 321000 | |

| 2000-12-16 | 354000 | |

| 2000-12-23 | 364000 | |

| 2000-12-30 | 353000 | |

| 2001-01-06 | 337000 | |

| 2001-01-13 | 318000 | |

| 2001-01-20 | 343000 | |

| 2001-01-27 | 362000 | |

| 2001-02-03 | 376000 | |

| 2001-02-10 | 365000 | |

| 2001-02-17 | 358000 | |

| 2001-02-24 | 386000 | |

| 2001-03-03 | 384000 | |

| 2001-03-10 | 393000 | |

| 2001-03-17 | 393000 | |

| 2001-03-24 | 378000 | |

| 2001-03-31 | 388000 | |

| 2001-04-07 | 398000 | |

| 2001-04-14 | 383000 | |

| 2001-04-21 | 400000 | |

| 2001-04-28 | 406000 | |

| 2001-05-05 | 381000 | |

| 2001-05-12 | 390000 | |

| 2001-05-19 | 402000 | |

| 2001-05-26 | 405000 | |

| 2001-06-02 | 406000 | |

| 2001-06-09 | 411000 | |

| 2001-06-16 | 394000 | |

| 2001-06-23 | 381000 | |

| 2001-06-30 | 394000 | |

| 2001-07-07 | 401000 | |

| 2001-07-14 | 405000 | |

| 2001-07-21 | 398000 | |

| 2001-07-28 | 388000 | |

| 2001-08-04 | 401000 | |

| 2001-08-11 | 394000 | |

| 2001-08-18 | 402000 | |

| 2001-08-25 | 395000 | |

| 2001-09-01 | 402000 | |

| 2001-09-08 | 408000 | |

| 2001-09-15 | 395000 | |

| 2001-09-22 | 453000 | |

| 2001-09-29 | 517000 | |

| 2001-10-06 | 476000 | |

| 2001-10-13 | 482000 | |

| 2001-10-20 | 482000 | |

| 2001-10-27 | 483000 | |

| 2001-11-03 | 440000 | |

| 2001-11-10 | 428000 | |

| 2001-11-17 | 431000 | |

| 2001-11-24 | 491000 | |

| 2001-12-01 | 465000 | |

| 2001-12-08 | 393000 | |

| 2001-12-15 | 389000 | |

| 2001-12-22 | 416000 | |

| 2001-12-29 | 421000 | |

| 2002-01-05 | 397000 | |

| 2002-01-12 | 418000 | |

| 2002-01-19 | 405000 | |

| 2002-01-26 | 414000 | |

| 2002-02-02 | 404000 | |

| 2002-02-09 | 397000 | |

| 2002-02-16 | 397000 | |

| 2002-02-23 | 398000 | |

| 2002-03-02 | 392000 | |

| 2002-03-09 | 399000 | |

| 2002-03-16 | 392000 | |

| 2002-03-23 | 415000 | |

| 2002-03-30 | 479000 | |

| 2002-04-06 | 445000 | |

| 2002-04-13 | 442000 | |

| 2002-04-20 | 416000 | |

| 2002-04-27 | 414000 | |

| 2002-05-04 | 409000 | |

| 2002-05-11 | 413000 | |

| 2002-05-18 | 411000 | |

| 2002-05-25 | 403000 | |

| 2002-06-01 | 378000 | |

| 2002-06-08 | 388000 | |

| 2002-06-15 | 396000 | |

| 2002-06-22 | 388000 | |

| 2002-06-29 | 386000 | |

| 2002-07-06 | 391000 | |

| 2002-07-13 | 384000 | |

| 2002-07-20 | 379000 | |

| 2002-07-27 | 390000 | |

| 2002-08-03 | 388000 | |

| 2002-08-10 | 389000 | |

| 2002-08-17 | 399000 | |

| 2002-08-24 | 398000 | |

| 2002-08-31 | 394000 | |

| 2002-09-07 | 416000 | |

| 2002-09-14 | 412000 | |

| 2002-09-21 | 401000 | |

| 2002-09-28 | 409000 | |

| 2002-10-05 | 404000 | |

| 2002-10-12 | 405000 | |

| 2002-10-19 | 412000 | |

| 2002-10-26 | 409000 | |

| 2002-11-02 | 405000 | |

| 2002-11-09 | 400000 | |

| 2002-11-16 | 389000 | |

| 2002-11-23 | 390000 | |

| 2002-11-30 | 377000 | |

| 2002-12-07 | 425000 | |

| 2002-12-14 | 429000 | |

| 2002-12-21 | 394000 | |

| 2002-12-28 | 409000 | |

| 2003-01-04 | 393000 | |

| 2003-01-11 | 378000 | |

| 2003-01-18 | 402000 | |

| 2003-01-25 | 407000 | |

| 2003-02-01 | 413000 | |

| 2003-02-08 | 390000 | |

| 2003-02-15 | 420000 | |

| 2003-02-22 | 421000 | |

| 2003-03-01 | 436000 | |

| 2003-03-08 | 424000 | |

| 2003-03-15 | 430000 | |

| 2003-03-22 | 411000 | |

| 2003-03-29 | 436000 | |

| 2003-04-05 | 417000 | |

| 2003-04-12 | 434000 | |

| 2003-04-19 | 450000 | |

| 2003-04-26 | 444000 | |

| 2003-05-03 | 428000 | |

| 2003-05-10 | 417000 | |

| 2003-05-17 | 425000 | |

| 2003-05-24 | 419000 | |

| 2003-05-31 | 431000 | |

| 2003-06-07 | 429000 | |

| 2003-06-14 | 421000 | |

| 2003-06-21 | 408000 | |

| 2003-06-28 | 429000 | |

| 2003-07-05 | 433000 | |

| 2003-07-12 | 412000 | |

| 2003-07-19 | 403000 | |

| 2003-07-26 | 398000 | |

| 2003-08-02 | 401000 | |

| 2003-08-09 | 404000 | |

| 2003-08-16 | 398000 | |

| 2003-08-23 | 391000 | |

| 2003-08-30 | 407000 | |

| 2003-09-06 | 422000 | |

| 2003-09-13 | 394000 | |

| 2003-09-20 | 379000 | |

| 2003-09-27 | 387000 | |

| 2003-10-04 | 386000 | |

| 2003-10-11 | 376000 | |

| 2003-10-18 | 387000 | |

| 2003-10-25 | 379000 | |

| 2003-11-01 | 363000 | |

| 2003-11-08 | 371000 | |

| 2003-11-15 | 370000 | |

| 2003-11-22 | 354000 | |

| 2003-11-29 | 357000 | |

| 2003-12-06 | 367000 | |

| 2003-12-13 | 363000 | |

| 2003-12-20 | 354000 | |

| 2003-12-27 | 349000 | |

| 2004-01-03 | 356000 | |

| 2004-01-10 | 354000 | |

| 2004-01-17 | 362000 | |

| 2004-01-24 | 353000 | |

| 2004-01-31 | 376000 | |

| 2004-02-07 | 380000 | |

| 2004-02-14 | 356000 | |

| 2004-02-21 | 359000 | |

| 2004-02-28 | 348000 | |

| 2004-03-06 | 344000 | |

| 2004-03-13 | 338000 | |

| 2004-03-20 | 346000 | |

| 2004-03-27 | 340000 | |

| 2004-04-03 | 335000 | |

| 2004-04-10 | 355000 | |

| 2004-04-17 | 364000 | |

| 2004-04-24 | 339000 | |

| 2004-05-01 | 324000 | |

| 2004-05-08 | 329000 | |

| 2004-05-15 | 349000 | |

| 2004-05-22 | 342000 | |

| 2004-05-29 | 337000 | |

| 2004-06-05 | 355000 | |

| 2004-06-12 | 339000 | |

| 2004-06-19 | 354000 | |

| 2004-06-26 | 348000 | |

| 2004-07-03 | 326000 | |

| 2004-07-10 | 345000 | |

| 2004-07-17 | 355000 | |

| 2004-07-24 | 348000 | |

| 2004-07-31 | 341000 | |

| 2004-08-07 | 336000 | |

| 2004-08-14 | 332000 | |

| 2004-08-21 | 343000 | |

| 2004-08-28 | 352000 | |

| 2004-09-04 | 326000 | |

| 2004-09-11 | 331000 | |

| 2004-09-18 | 341000 | |

| 2004-09-25 | 351000 | |

| 2004-10-02 | 335000 | |

| 2004-10-09 | 338000 | |

| 2004-10-16 | 327000 | |

| 2004-10-23 | 338000 | |

| 2004-10-30 | 332000 | |

| 2004-11-06 | 330000 | |

| 2004-11-13 | 337000 | |

| 2004-11-20 | 313000 | |

| 2004-11-27 | 335000 | |

| 2004-12-04 | 343000 | |

| 2004-12-11 | 316000 | |

| 2004-12-18 | 322000 | |

| 2004-12-25 | 320000 | |

| 2005-01-01 | 356000 | |

| 2005-01-08 | 369000 | |

| 2005-01-15 | 332000 | |

| 2005-01-22 | 329000 | |

| 2005-01-29 | 331000 | |

| 2005-02-05 | 307000 | |

| 2005-02-12 | 308000 | |

| 2005-02-19 | 318000 | |

| 2005-02-26 | 314000 | |

| 2005-03-05 | 333000 | |

| 2005-03-12 | 324000 | |

| 2005-03-19 | 329000 | |

| 2005-03-26 | 342000 | |

| 2005-04-02 | 335000 | |

| 2005-04-09 | 323000 | |

| 2005-04-16 | 307000 | |

| 2005-04-23 | 317000 | |

| 2005-04-30 | 334000 | |

| 2005-05-07 | 327000 | |

| 2005-05-14 | 321000 | |

| 2005-05-21 | 320000 | |

| 2005-05-28 | 340000 | |

| 2005-06-04 | 338000 | |

| 2005-06-11 | 333000 | |

| 2005-06-18 | 321000 | |

| 2005-06-25 | 311000 | |

| 2005-07-02 | 327000 | |

| 2005-07-09 | 338000 | |

| 2005-07-16 | 323000 | |

| 2005-07-23 | 318000 | |

| 2005-07-30 | 316000 | |

| 2005-08-06 | 311000 | |

| 2005-08-13 | 319000 | |

| 2005-08-20 | 315000 | |

| 2005-08-27 | 318000 | |

| 2005-09-03 | 326000 | |

| 2005-09-10 | 422000 | |

| 2005-09-17 | 424000 | |

| 2005-09-24 | 359000 | |

| 2005-10-01 | 384000 | |

| 2005-10-08 | 383000 | |

| 2005-10-15 | 348000 | |

| 2005-10-22 | 324000 | |

| 2005-10-29 | 322000 | |

| 2005-11-05 | 325000 | |

| 2005-11-12 | 309000 | |

| 2005-11-19 | 324000 | |

| 2005-11-26 | 311000 | |

| 2005-12-03 | 321000 | |

| 2005-12-10 | 327000 | |

| 2005-12-17 | 312000 | |

| 2005-12-24 | 320000 | |

| 2005-12-31 | 302000 | |

| 2006-01-07 | 326000 | |

| 2006-01-14 | 285000 | |

| 2006-01-21 | 290000 | |

| 2006-01-28 | 282000 | |

| 2006-02-04 | 289000 | |

| 2006-02-11 | 298000 | |

| 2006-02-18 | 283000 | |

| 2006-02-25 | 293000 | |

| 2006-03-04 | 302000 | |

| 2006-03-11 | 307000 | |

| 2006-03-18 | 303000 | |

| 2006-03-25 | 295000 | |

| 2006-04-01 | 291000 | |

| 2006-04-08 | 299000 | |

| 2006-04-15 | 299000 | |

| 2006-04-22 | 308000 | |

| 2006-04-29 | 321000 | |

| 2006-05-06 | 347000 | |

| 2006-05-13 | 335000 | |

| 2006-05-20 | 319000 | |

| 2006-05-27 | 330000 | |

| 2006-06-03 | 307000 | |

| 2006-06-10 | 298000 | |

| 2006-06-17 | 308000 | |

| 2006-06-24 | 309000 | |

| 2006-07-01 | 316000 | |

| 2006-07-08 | 343000 | |

| 2006-07-15 | 318000 | |

| 2006-07-22 | 306000 | |

| 2006-07-29 | 311000 | |

| 2006-08-05 | 318000 | |

| 2006-08-12 | 310000 | |

| 2006-08-19 | 315000 | |

| 2006-08-26 | 314000 | |

| 2006-09-02 | 315000 | |

| 2006-09-09 | 314000 | |

| 2006-09-16 | 324000 | |

| 2006-09-23 | 319000 | |

| 2006-09-30 | 309000 | |

| 2006-10-07 | 316000 | |

| 2006-10-14 | 305000 | |

| 2006-10-21 | 313000 | |

| 2006-10-28 | 328000 | |

| 2006-11-04 | 319000 | |

| 2006-11-11 | 311000 | |

| 2006-11-18 | 326000 | |

| 2006-11-25 | 349000 | |

| 2006-12-02 | 327000 | |

| 2006-12-09 | 311000 | |

| 2006-12-16 | 318000 | |

| 2006-12-23 | 323000 | |

| 2006-12-30 | 341000 | |

| 2007-01-06 | 330000 | |

| 2007-01-13 | 296000 | |

| 2007-01-20 | 335000 | |

| 2007-01-27 | 308000 | |

| 2007-02-03 | 310000 | |

| 2007-02-10 | 338000 | |

| 2007-02-17 | 321000 | |

| 2007-02-24 | 322000 | |

| 2007-03-03 | 320000 | |

| 2007-03-10 | 308000 | |

| 2007-03-17 | 309000 | |

| 2007-03-24 | 303000 | |

| 2007-03-31 | 307000 | |

| 2007-04-07 | 332000 | |

| 2007-04-14 | 327000 | |

| 2007-04-21 | 321000 | |

| 2007-04-28 | 301000 | |

| 2007-05-05 | 300000 | |

| 2007-05-12 | 297000 | |

| 2007-05-19 | 310000 | |

| 2007-05-26 | 310000 | |

| 2007-06-02 | 313000 | |

| 2007-06-09 | 313000 | |

| 2007-06-16 | 320000 | |

| 2007-06-23 | 313000 | |

| 2007-06-30 | 317000 | |

| 2007-07-07 | 321000 | |

| 2007-07-14 | 317000 | |

| 2007-07-21 | 310000 | |

| 2007-07-28 | 305000 | |

| 2007-08-04 | 314000 | |

| 2007-08-11 | 316000 | |

| 2007-08-18 | 321000 | |

| 2007-08-25 | 329000 | |

| 2007-09-01 | 314000 | |

| 2007-09-08 | 321000 | |

| 2007-09-15 | 313000 | |

| 2007-09-22 | 302000 | |

| 2007-09-29 | 317000 | |

| 2007-10-06 | 316000 | |

| 2007-10-13 | 335000 | |

| 2007-10-20 | 334000 | |

| 2007-10-27 | 328000 | |

| 2007-11-03 | 327000 | |

| 2007-11-10 | 333000 | |

| 2007-11-17 | 332000 | |

| 2007-11-24 | 352000 | |

| 2007-12-01 | 344000 | |

| 2007-12-08 | 332000 | |

| 2007-12-15 | 350000 | |

| 2007-12-22 | 355000 | |

| 2007-12-29 | 360000 | |

| 2008-01-05 | 346000 | |

| 2008-01-12 | 322000 | |

| 2008-01-19 | 321000 | |

| 2008-01-26 | 366000 | |

| 2008-02-02 | 350000 | |

| 2008-02-09 | 344000 | |

| 2008-02-16 | 339000 | |

| 2008-02-23 | 354000 | |

| 2008-03-01 | 345000 | |

| 2008-03-08 | 348000 | |

| 2008-03-15 | 369000 | |

| 2008-03-22 | 368000 | |

| 2008-03-29 | 387000 | |

| 2008-04-05 | 354000 | |

| 2008-04-12 | 365000 | |

| 2008-04-19 | 349000 | |

| 2008-04-26 | 370000 | |

| 2008-05-03 | 370000 | |

| 2008-05-10 | 366000 | |

| 2008-05-17 | 367000 | |

| 2008-05-24 | 369000 | |

| 2008-05-31 | 362000 | |

| 2008-06-07 | 382000 | |

| 2008-06-14 | 378000 | |

| 2008-06-21 | 381000 | |

| 2008-06-28 | 392000 | |

| 2008-07-05 | 371000 | |

| 2008-07-12 | 385000 | |

| 2008-07-19 | 402000 | |

| 2008-07-26 | 434000 | |

| 2008-08-02 | 448000 | |

| 2008-08-09 | 430000 | |

| 2008-08-16 | 424000 | |

| 2008-08-23 | 421000 | |

| 2008-08-30 | 442000 | |

| 2008-09-06 | 441000 | |

| 2008-09-13 | 449000 | |

| 2008-09-20 | 483000 | |

| 2008-09-27 | 483000 | |

| 2008-10-04 | 482000 | |

| 2008-10-11 | 461000 | |

| 2008-10-18 | 478000 | |

| 2008-10-25 | 480000 | |

| 2008-11-01 | 490000 | |

| 2008-11-08 | 512000 | |

| 2008-11-15 | 536000 | |

| 2008-11-22 | 532000 | |

| 2008-11-29 | 529000 | |

| 2008-12-06 | 570000 | |

| 2008-12-13 | 566000 | |

| 2008-12-20 | 587000 | |

| 2008-12-27 | 533000 | |

| 2009-01-03 | 503000 | |

| 2009-01-10 | 551000 | |

| 2009-01-17 | 591000 | |

| 2009-01-24 | 586000 | |

| 2009-01-31 | 629000 | |

| 2009-02-07 | 637000 | |

| 2009-02-14 | 632000 | |

| 2009-02-21 | 655000 | |

| 2009-02-28 | 652000 | |

| 2009-03-07 | 660000 | |

| 2009-03-14 | 651000 | |

| 2009-03-21 | 661000 | |

| 2009-03-28 | 665000 | |

| 2009-04-04 | 653000 | |

| 2009-04-11 | 599000 | |

| 2009-04-18 | 639000 | |

| 2009-04-25 | 620000 | |

| 2009-05-02 | 602000 | |

| 2009-05-09 | 625000 | |

| 2009-05-16 | 620000 | |

| 2009-05-23 | 606000 | |

| 2009-05-30 | 607000 | |

| 2009-06-06 | 596000 | |

| 2009-06-13 | 595000 | |

| 2009-06-20 | 608000 | |

| 2009-06-27 | 594000 | |

| 2009-07-04 | 573000 | |

| 2009-07-11 | 546000 | |

| 2009-07-18 | 560000 | |

| 2009-07-25 | 587000 | |

| 2009-08-01 | 555000 | |

| 2009-08-08 | 555000 | |

| 2009-08-15 | 562000 | |

| 2009-08-22 | 560000 | |

| 2009-08-29 | 564000 | |

| 2009-09-05 | 558000 | |

| 2009-09-12 | 542000 | |

| 2009-09-19 | 536000 | |

| 2009-09-26 | 554000 | |

| 2009-10-03 | 533000 | |

| 2009-10-10 | 511000 | |

| 2009-10-17 | 531000 | |

| 2009-10-24 | 530000 | |

| 2009-10-31 | 522000 | |

| 2009-11-07 | 512000 | |

| 2009-11-14 | 507000 | |

| 2009-11-21 | 482000 | |

| 2009-11-28 | 475000 | |

| 2009-12-05 | 497000 | |

| 2009-12-12 | 498000 | |

| 2009-12-19 | 479000 | |

| 2009-12-26 | 468000 | |

| 2010-01-02 | 456000 | |

| 2010-01-09 | 469000 | |

| 2010-01-16 | 507000 | |

| 2010-01-23 | 471000 | |

| 2010-01-30 | 496000 | |

| 2010-02-06 | 466000 | |

| 2010-02-13 | 489000 | |

| 2010-02-20 | 500000 | |

| 2010-02-27 | 488000 | |

| 2010-03-06 | 472000 | |

| 2010-03-13 | 478000 | |

| 2010-03-20 | 472000 | |

| 2010-03-27 | 459000 | |

| 2010-04-03 | 479000 | |

| 2010-04-10 | 479000 | |

| 2010-04-17 | 469000 | |

| 2010-04-24 | 449000 | |

| 2010-05-01 | 451000 | |

| 2010-05-08 | 451000 | |

| 2010-05-15 | 474000 | |

| 2010-05-22 | 463000 | |

| 2010-05-29 | 458000 | |

| 2010-06-05 | 459000 | |

| 2010-06-12 | 467000 | |

| 2010-06-19 | 452000 | |

| 2010-06-26 | 464000 | |

| 2010-07-03 | 454000 | |

| 2010-07-10 | 439000 | |

| 2010-07-17 | 462000 | |

| 2010-07-24 | 465000 | |

| 2010-07-31 | 476000 | |

| 2010-08-07 | 483000 | |

| 2010-08-14 | 486000 | |

| 2010-08-21 | 464000 | |

| 2010-08-28 | 467000 | |

| 2010-09-04 | 452000 | |

| 2010-09-11 | 444000 | |

| 2010-09-18 | 459000 | |

| 2010-09-25 | 459000 | |

| 2010-10-02 | 446000 | |

| 2010-10-09 | 459000 | |

| 2010-10-16 | 444000 | |

| 2010-10-23 | 432000 | |

| 2010-10-30 | 453000 | |

| 2010-11-06 | 434000 | |

| 2010-11-13 | 432000 | |

| 2010-11-20 | 407000 | |

| 2010-11-27 | 432000 | |

| 2010-12-04 | 428000 | |

| 2010-12-11 | 425000 | |

| 2010-12-18 | 424000 | |

| 2010-12-25 | 404000 | |

| 2011-01-01 | 413000 | |

| 2011-01-08 | 434000 | |

| 2011-01-15 | 421000 | |

| 2011-01-22 | 446000 | |

| 2011-01-29 | 420000 | |

| 2011-02-05 | 402000 | |

| 2011-02-12 | 425000 | |

| 2011-02-19 | 394000 | |

| 2011-02-26 | 385000 | |

| 2011-03-05 | 414000 | |

| 2011-03-12 | 404000 | |

| 2011-03-19 | 407000 | |

| 2011-03-26 | 399000 | |

| 2011-04-02 | 395000 | |

| 2011-04-09 | 416000 | |

| 2011-04-16 | 402000 | |

| 2011-04-23 | 422000 | |

| 2011-04-30 | 468000 | |

| 2011-05-07 | 435000 | |

| 2011-05-14 | 414000 | |

| 2011-05-21 | 423000 | |

| 2011-05-28 | 418000 | |

| 2011-06-04 | 423000 | |

| 2011-06-11 | 413000 | |

| 2011-06-18 | 416000 | |

| 2011-06-25 | 421000 | |

| 2011-07-02 | 418000 | |

| 2011-07-09 | 408000 | |

| 2011-07-16 | 420000 | |

| 2011-07-23 | 411000 | |

| 2011-07-30 | 406000 | |

| 2011-08-06 | 405000 | |

| 2011-08-13 | 409000 | |

| 2011-08-20 | 415000 | |

| 2011-08-27 | 409000 | |

| 2011-09-03 | 414000 | |

| 2011-09-10 | 429000 | |

| 2011-09-17 | 422000 | |

| 2011-09-24 | 406000 | |

| 2011-10-01 | 405000 | |

| 2011-10-08 | 410000 | |

| 2011-10-15 | 395000 | |

| 2011-10-22 | 403000 | |

| 2011-10-29 | 399000 | |

| 2011-11-05 | 392000 | |

| 2011-11-12 | 383000 | |

| 2011-11-19 | 385000 | |

| 2011-11-26 | 397000 | |

| 2011-12-03 | 387000 | |